As crypto cards (commonly referred to as “U Cards”) gradually expand into more everyday spending scenarios—from online subscriptions and cross-border shopping to travel expenses and remote work payments—they are evolving from a niche Web3 tool into a more mainstream payment option.

This naturally raises a question: if traditional debit cards are already widely adopted, why are more and more users choosing crypto cards?

The answer is not simply because “crypto” is a new and attractive concept, but because users’ asset structures and payment behaviors have fundamentally changed. According to an Artemis industry report, by the end of 2025, monthly spending through crypto cards had exceeded $1.5 billion, reaching an annualized scale of approximately $18 billion, growing from around $100 million per month in early 2023. This represents a compound annual growth rate (CAGR) of 106%.

As stablecoins such as USDT and USDC become an increasingly common way for users to hold and manage assets, crypto cards make it possible to use these on-chain assets more directly in real-world spending.

Users no longer need to frequently move funds between wallets, exchanges, and bank accounts. Instead, they can directly spend stablecoins in supported scenarios for online subscriptions, cross-border shopping, travel expenses, and digital services.

For many Web3 users, remote workers, and cross-border consumers, crypto cards shorten the path from assets to spending and create a payment experience that is closer to how they already manage their funds.

Crypto Cards vs Traditional Debit Cards: Basic Definitions

Before comparing the two, let’s first clarify some core concepts.

What Is a Traditional Debit Card?

A traditional debit card is the type of bank card most people use in their daily lives. It is directly linked to a bank account, where funds are held in fiat currency (government-issued currencies such as RMB, USD, or EUR). When a payment is made, the bank system deducts funds directly from the account balance. Debit cards are widely used for everyday spending, salary deposits, transfers, and general account management.

What Is a Crypto Card?

A crypto card is a type of payment card that allows users to spend digital assets—such as stablecoins—in everyday transactions. It is typically issued through regulated settlement platforms in partnership with card networks like Visa or Mastercard.

Many users assume that when paying with a crypto card, merchants directly receive USDT or USDC. In reality, most merchants still only settle in fiat currencies such as USD or EUR.

When a transaction occurs, the system automatically converts stablecoins into the corresponding fiat currency in real time and completes the payment through the Visa or Mastercard network. In essence, a crypto card acts as a bridge between on-chain assets and the traditional payment system, rather than enabling merchants to directly accept cryptocurrency.

What Are The Differences Between Crypto Cards And Traditional Debit Cards? 5 Core Dimensions

At first glance, crypto cards and traditional debit cards look quite similar. However, once you break down their underlying structures, the differences become significant.

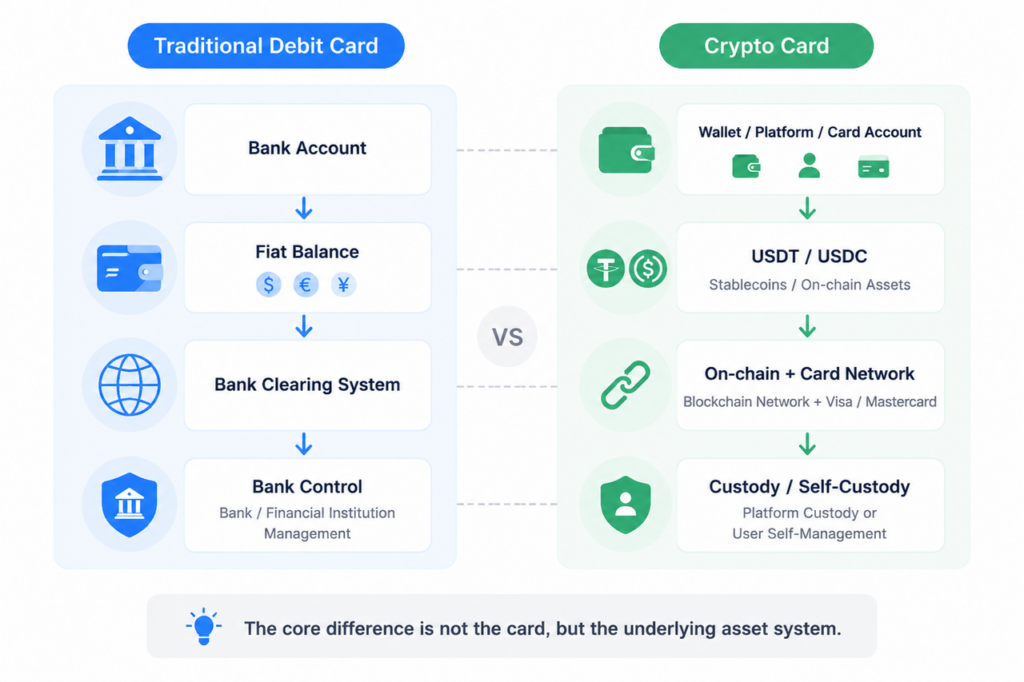

- Asset source: fiat balances vs stablecoins / on-chain assets

Traditional debit cards are funded by fiat balances held in a bank account. When users make a payment, the transaction is processed and settled within the traditional financial system.

Crypto cards, on the other hand, are typically funded by stablecoins such as USDT or USDC, or other supported on-chain assets.

This is the most fundamental difference: traditional debit cards are designed for fiat-based banking users, while crypto cards are designed for on-chain asset holders.

- Account structure: bank accounts vs wallets / card accounts / platform accounts

Traditional debit cards are directly linked to a bank account. Funds are stored in the bank account, and the bank handles balance deduction, payment authorization, and transaction records.

Crypto card systems are more complex. Assets may be held in a self-custodial wallet, a centralized exchange account, a platform account, or a dedicated card account. The structure varies significantly depending on the product design—especially in terms of where assets are stored, who controls them, and which account is debited during spending.

For example, some crypto cards use a platform balance as the spending source, while others are designed around self-custody models that allow users to retain control of their wallet assets while still accessing traditional payment networks.

For this reason, users should not only check whether a card supports USDT or USDC, but also understand its underlying account architecture.

- Settlement flow: traditional financial clearing vs on-chain-to-fiat conversion

Traditional debit card payments follow a relatively straightforward process. After a card is swiped, the transaction is authorized, cleared, and settled through issuers, card networks, acquiring banks, and merchants—all within the fiat financial system.

Crypto cards add an additional conversion layer. They must bridge on-chain assets with traditional card networks.

In other words, traditional debit cards handle “how bank balances are paid to merchants,” while crypto cards handle “how on-chain assets are converted into a payment format accepted by merchants.”

This is why user experience can vary significantly across different crypto card products—factors such as manual conversion requirements, multi-chain support, and integration efficiency all affect the final payment experience.

- Control model: bank-managed accounts vs custodial / self-custodial structures

Traditional debit card funds are held within a bank account. Account management, transaction controls, risk systems, and fund security are handled by the bank or regulated financial institutions. Users have usage rights, but not full control over the account infrastructure.

Crypto cards differ depending on their custody model.

Some operate under a custodial structure, where users deposit assets into a platform or exchange account before spending via the card. This model is easier to use but does not give users direct control of private keys.

Others adopt a self-custody approach, where users retain control of their wallet keys and assets, while the platform provides access to payment networks without long-term custody of funds.

Therefore, the key difference is not only the type of asset, but also the level of control users have over their funds.

- Compliance requirements: banking regulation vs layered KYC/AML and network rules

Traditional debit cards are governed by banks, card issuers, card networks, anti-money laundering (AML) rules, and local financial regulations. Users may face restrictions during account opening, cross-border spending, or large transactions depending on banking policies.

Crypto cards are also subject to compliance requirements—often in a more layered structure. These may include KYC (Know Your Customer) and AML checks, on-chain source-of-funds verification, issuer rules, BIN restrictions (the first digits of a card number that determine issuing region/type), merchant category restrictions, regional policies, and card network rules.

This means crypto cards are not a way to bypass traditional financial regulations. They still operate within regulated payment networks and must comply with local laws. The only difference is that the funding source shifts from bank-held fiat to stablecoins or on-chain assets.

As a result, users should not only evaluate supported tokens, but also consider KYC requirements, available regions, merchant acceptance, fee structures, and restricted use cases.

Crypto Card vs Traditional Bank Debit Card Comparison Table

| Dimension | Traditional Debit Card | Crypto Card |

| Asset type | Fiat currency held in a bank account | Stablecoins such as USDT, USDC, or other on-chain assets |

| Account structure | Bank account management | Wallets, platform accounts, exchange accounts, or dedicated card accounts |

| Settlement flow | Bank account → card network → merchant | On-chain assets / stablecoins → crypto card → card network → merchant |

| Control model | Managed by banks or financial institutions | Depends on product design; either custodial or self-custodial |

| Compliance requirements | Banking regulations, issuer rules, local financial regulations | KYC/AML, on-chain source-of-funds checks, regional policies, BIN rules, merchant restrictions |

| Risk & limitations | Primarily banking risk controls and potential account freezes | May include regional restrictions, BIN-based limitations, funding/compliance constraints |

| Target users | Local bank users, salary account holders, everyday fiat consumers | Web3 users, stablecoin holders, remote workers, cross-border consumers |

Therefore, crypto cards are not simply a “replacement” for traditional bank cards, but rather a new payment layer designed for a different type of asset structure and spending behavior.

Who Is A Traditional Debit Card Suitable For? And Why Is It Still The Dominant Payment Tool

Traditional debit cards remain a highly reliable payment method.

For local consumption, salary payments, daily bills, in-store purchases, and bank account management, they are efficient, familiar, and widely accepted.

However, as users’ payment scenarios become increasingly global, certain structural limitations are becoming more apparent.

For example, when users make cross-border payments, traditional debit cards may involve foreign exchange conversion fees, international transaction fees, exchange rate spreads, issuing bank rules, and regional risk controls. The rules across different banks, countries, and payment networks are not fully consistent, making it difficult for users to accurately predict the final cost of each transaction.

In addition, the movement of funds via traditional debit cards relies heavily on banking infrastructure. Cross-border transfers, overseas spending, international subscriptions, and multi-currency payments often need to comply with banking system operating hours, foreign exchange policies, and account restrictions.

These are not “defects” of debit cards, but rather the structural design of the traditional financial system itself.

Traditional debit cards are naturally suited for local fiat-based accounts and stable banking services. However, when users’ assets are no longer confined to bank accounts, they may not always represent the shortest or most direct payment path.

What Are The Advantages Of Crypto Cards? Why Are More People Starting To Use U Cards?

Crypto cards are often simply understood as “using cryptocurrency for payments.” However, from a user experience perspective, what they truly change is not just the payment asset itself, but the entire path from assets to spending.

- Shorter payment path

For users who already hold stablecoins or on-chain assets, traditional spending usually requires multiple steps, such as selling assets, withdrawing to a bank account, and then completing payments via a debit card.

Crypto cards offer an alternative path: users can directly connect eligible assets to real-world payment scenarios and spend at supported merchants, reducing the need to move funds across multiple wallets, platforms, and banking systems.

For users who already manage assets on-chain, this approach is typically smoother and aligns more naturally with their existing financial behavior.

- More predictable cross-border costs

Cross-border payments often involve exchange rate conversions, international transaction fees, and different fee structures across banks and regions.

For stablecoin users, funds are usually denominated in USD-pegged assets, which makes it easier to estimate actual spending when paying for overseas subscriptions, international shopping, or cross-border services.

Crypto cards do not eliminate fees entirely, nor are they always cheaper than traditional bank cards. However, they can reduce the uncertainty caused by repeated conversions and multi-step fund transfers, making the payment path more transparent and predictable.

- More unified asset management and payment experience

Traditional debit cards are primarily built around bank accounts. In contrast, many Web3 users now manage their assets in wallets and on-chain ecosystems.

Some crypto card products are starting to integrate asset management, yield strategies, and real-world spending into a single system, allowing users to avoid constantly switching between wallets, exchanges, banks, and payment tools.

For users holding digital assets long-term, this integrated experience can reduce operational friction and make asset usage more seamless and continuous.

Who Is More Suitable To Use Crypto Cards (U Cards)?

When discussing crypto cards and traditional debit cards, a common misconception is to treat them as direct competitors:

- Are traditional cards becoming obsolete?

- Are crypto cards always better?

- Will everyone eventually switch to crypto cards?

In reality, they serve different asset structures and spending behaviors.

If your income is primarily deposited into a bank account and your spending mostly happens in a local fiat currency environment, then traditional debit cards are still the most natural and stable choice.

However, crypto cards are often a better fit if you fall into one or more of the following categories:

- Your income is mainly received in stablecoins such as USDT or USDC;

- You frequently work in Web3 projects or receive payments from overseas clients;

- You hold digital assets long-term and want to reduce the steps of selling, withdrawing, and converting currencies;

- You often make cross-border payments, pay for overseas subscriptions, or travel internationally;

- You prefer more flexibility between asset management and everyday spending.

For these users, crypto cards are not meant to replace traditional bank cards, but to provide a smoother way for on-chain assets to flow into real-world spending scenarios.

Why Are Crypto Cards Better Suited for Cross-Border Payments, Overseas Subscriptions, and Global Spending Scenarios?

As more users earn income through Web3 projects, remote work, or digital assets, the value of crypto cards is becoming increasingly evident in real-world spending scenarios.

Case 1: How a remote developer directly spends USDT income

Tim works long-term for overseas projects, and his income is mainly settled in USDT.

In the past, he had to first transfer USDT to an exchange, convert it into fiat currency, withdraw it to a bank account, and then use a debit card for daily spending. This process involves multiple steps across wallets, exchanges, and banking systems.

After using a crypto card, he can directly connect stablecoins to payment scenarios and use them for everyday expenses such as groceries, dining, and online purchases. For users who already hold stablecoins, the path from income to spending becomes significantly more direct.

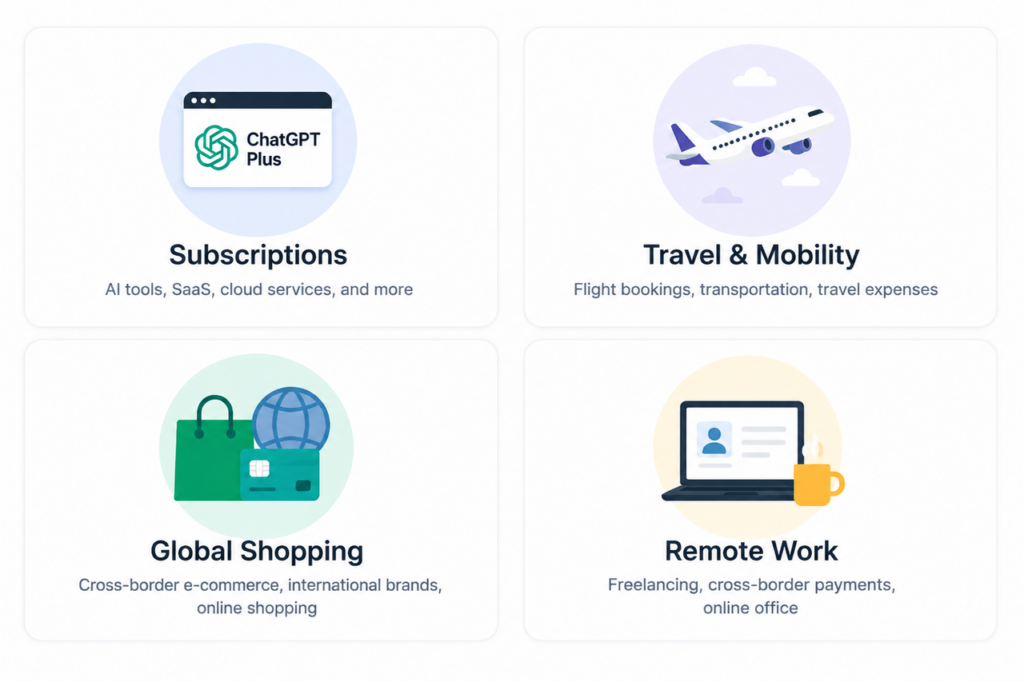

Case 2: How a heavy AI tools user pays for overseas SaaS

David is a heavy user of AI tools and subscribes monthly to services such as ChatGPT Plus, Midjourney, and various cloud services.

Due to restrictions related to card issuing regions, card types, or payment networks, traditional bank cards sometimes fail when paying on overseas platforms.

With a stablecoin-supported crypto card, he can directly use USDT or USDC from his account to complete subscription payments without repeatedly converting currencies or switching between multiple payment channels.

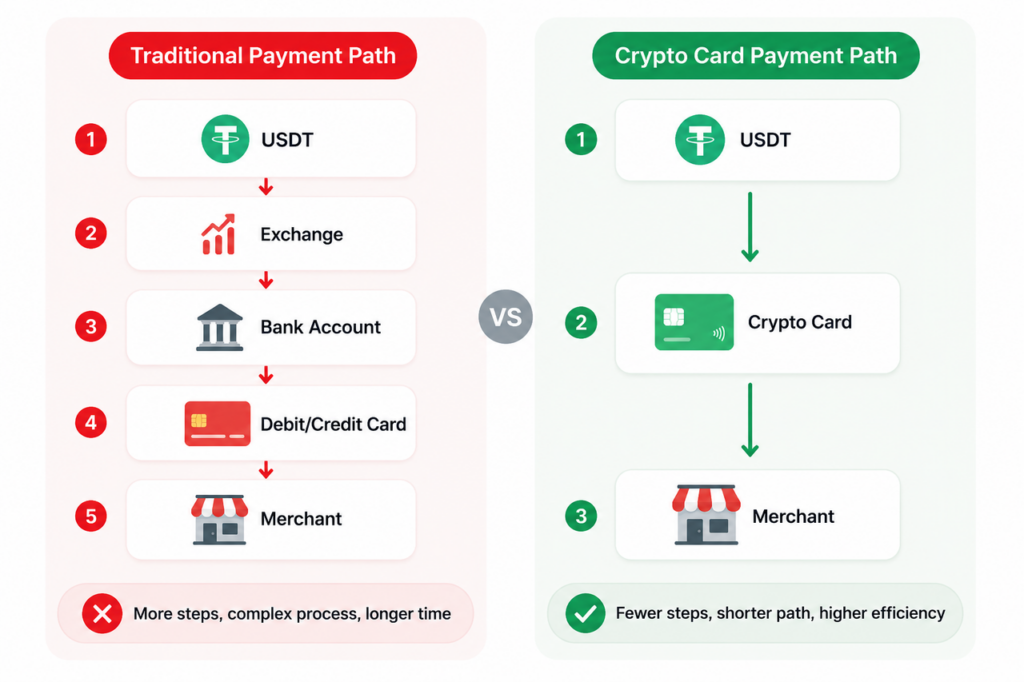

From on-chain assets to real-world spending: the path is getting shorter

The two cases above reflect a broader trend: income, assets, and spending behaviors are becoming increasingly global, while traditional payment systems are still primarily built around local bank accounts.

For users already holding stablecoins, the traditional payment path is often: Stablecoin → Exchange → Bank account → Debit card → Merchant.

Crypto cards simplify this into: Stablecoin → Crypto card → Merchant.

Crypto cards are not necessarily suitable for everyone, but for the following groups, they often provide a smoother payment experience:

- Stablecoin holders: those who want to directly use USDT or USDC for subscriptions, shopping, or travel without frequent conversions.

- Web3 professionals and remote workers: income comes from on-chain projects, DAOs, or overseas clients, requiring seamless access to real-world spending.

- Cross-border consumers and digital nomads: frequently pay for overseas SaaS tools, AI services, cloud services, hotels, and flights.

- Users who prioritize asset control: prefer reducing reliance on exchanges or centralized platforms while maintaining clearer separation between asset management and spending.

For common real-life scenarios such as overseas subscriptions, daily consumption, and cross-border payments, you can also refer to this practical guide: “Why is USDT daily spending so difficult? A complete breakdown of payment challenges and U-card solutions.”

Web3 Wallets + U Cards + DeFi Earn: How Crypto Payment Products Are Evolving

Early crypto cards were typically isolated products.

Users had to first transfer funds from a wallet to a platform account, then top up a card account, and only then could they use the card for payments. Asset management, yield management, and spending were largely separated.

While this model solved the basic problem of “can I spend crypto with a card?”, it did not necessarily reduce complexity. Users still had to switch between multiple apps, wallets, accounts, and payment flows.

As crypto payment products continue to evolve, more solutions are shifting from a single-card tool to a comprehensive Web3 financial gateway.

In other words, crypto cards are no longer just “a card product”— they are increasingly being integrated with wallets, multi-chain asset management, stablecoin top-ups, on-chain yield strategies, and real-world payment scenarios.

BenPay Card is one example of this trend.

BenPay Card: Making Stablecoins Easier to Use in Real-World Payments

For many users, hesitation around crypto cards does not come from a lack of understanding of crypto assets, but from concerns about user experience complexity.

What they care more about is:

- Whether it can directly connect to real-world spending scenarios;

- Whether they need to constantly switch between different accounts and apps;

- Whether asset management and payments can be unified in one place;

- Whether idle funds can still remain productive.

BenPay Card is designed to address exactly these concerns.

Users can create an account through the BenPay App, manage on-chain assets, and choose suitable card types based on their needs. After completing the required setup, they can connect supported assets such as USDT and USDC to the card for real-world spending, including online subscriptions, cross-border payments, travel expenses, and daily purchases.

Unlike traditional single-function card products, BenPay Card emphasizes an integrated experience.

Users do not need to separate asset management and payment tools into different systems. Instead, they can manage multi-chain assets, use cards, and arrange on-chain yield strategies within a single application.

For users who already hold stablecoins, this approach better aligns with their existing financial habits: assets remain on-chain, while still being seamlessly usable in real-world payments via the card.

BenPay Card also supports on-chain yield for card account balances. Through BenPay DeFi Earn, unused card balances can be allocated to selected mainstream DeFi protocols to generate yield, subject to product rules and risk disclosures, improving capital efficiency.

This makes BenPay Card not only a payment gateway, but also a comprehensive tool connecting stablecoin assets, on-chain yield, and real-world spending.

Conclusion: Choosing Between Crypto Cards And Traditional Debit Cards Depends On Asset Sources And Spending Scenarios

More and more people are choosing crypto cards, not because traditional debit cards are becoming less important. On the contrary, traditional debit cards will continue to exist for a long time, serving local bank accounts, fiat-based spending, and everyday payment scenarios.

What is truly changing is that an increasing number of users no longer hold all their assets inside bank accounts. As stablecoins, on-chain balances, and Web3 income become part of some users’ everyday financial reality, payment tools also need to evolve alongside where those assets are held.

Crypto cards are a reflection of this shift. They are not designed to replace all traditional bank cards, but to make on-chain assets more naturally usable in real-world payment networks. What they reduce is not the “bank card” itself, but the unnecessary friction of switching between wallets, exchanges, bank accounts, and payment tools.

For users exploring this transition, integrated solutions like BenPay Card provide a more complete path: managing assets in a single app, participating in on-chain yield, and connecting stablecoins directly to real-world spending scenarios.

In the future, the choice of payment tools may no longer depend on “which card is better,” but rather on where your assets are, where your spending happens, and which tool can connect the two with the shortest path.