You have USDT in your wallet, yet using it for everyday purchases—buying a coffee, paying for an online order, or covering an unexpected expense—feels surprisingly difficult. You want to subscribe to overseas services like ChatGPT Plus, Codex, Claude, Midjourney, or Netflix, but keep getting stuck at the payment step. You’re traveling abroad or working remotely, only to run into failed cross-border payments, excessive fees, or bank card blocks.

These may seem like isolated annoyances, but they all point to the same underlying issue: your USDT exists on-chain, while most spending scenarios still rely on bank cards, payment gateways, and local fiat settlement.

For users holding USDT or USDC, the real challenge isn’t whether they have a balance; it’s whether that balance can be directly used for subscriptions, shopping, travel, and everyday payments. This is precisely why U-cards (crypto payment cards / stablecoin payment cards) are drawing increasing attention.

This article breaks down three common scenarios—overseas subscriptions, everyday spending, and cross-border travel—to explain why USDT is still hard to spend and how U-cards offer a shorter bridge between on-chain assets and real-world payments.

Key takeaways:

- USDT/USDC is difficult to use directly for daily purchases because there remains a conversion gap between on-chain assets and traditional payment systems.

- Failed overseas subscriptions are often tied to card BINs, regional risk controls, recurring billing capabilities, and payment gateway rules.

- While C2C cashing out is feasible, it comes with issues like settlement timing, spreads, bank risk controls, and record-keeping complexity.

- U-cards don’t make every merchant accept USDT directly; instead, they connect stablecoin balances to the existing card payment network.

- A stablecoin payment card like BenPay Card suits users who want to reduce the steps of selling U, withdrawing funds, exchanging currencies, and linking cards.

Overseas Subscriptions: Why Does Payment Fail Even with USDT?

Many people first experience the frustration of “having USDT but struggling to spend it” not when shopping offline, but when subscribing to overseas services.

You want to sign up for AI tools like ChatGPT Plus, Claude Pro, Midjourney, or Codex; stream on Netflix or Spotify; or purchase overseas SaaS, cloud services, or AI APIs. Your wallet may already hold enough USDT or USDC, but when you reach the checkout page, there’s rarely a “Pay with USDT” button.

You still need to enter a bank card, credit card, or virtual card.

This is the first hurdle for stablecoin spending: your assets are on-chain, but overseas subscription platforms still accept payments primarily through the traditional card system.

- Why Can’t You Complete Overseas Subscriptions with USDT?

Overseas subscription platforms typically interface with international payment gateways and card networks. To these platforms, what matters is your card number, issuing region, card BIN, transaction IP, account region, recurring billing capability, and historical risk profile—not whether your on-chain wallet holds stablecoins.

So when stablecoin users want to subscribe to overseas services, the common paths often become:

- Sell USDT for fiat first, then pay with a bank card;

- Find a virtual card or prepaid card, top it up, and then subscribe;

- Use a third-party subscription service;

- Try different cards until one goes through.

These approaches can work in certain cases, but the experience is inconsistent. Overseas AI tools, streaming platforms, ad platforms, and developer services tend to have stricter requirements for subscription billing and payment risk control.

- Where Do Overseas Subscription Payments Typically Fail?

Payment failures aren’t necessarily due to insufficient balance or account issues. Often, the problem lies in the mismatch between the card and the platform’s payment rules.

Common causes include:

- The card BIN’s region doesn’t match the account region or IP location;

- The card is flagged as a prepaid or virtual card type with lower merchant acceptance;

- The card doesn’t support stable Card-on-File recurring billing;

- That BIN range has been associated with irregular transactions and carries a poor historical risk record;

- The platform is more sensitive to small-amount, high-frequency, cross-border, or auto-debit transactions;

- Card balance, expiration date, billing address, and other details are unstable.

This explains why some cards work for the first payment but fail on the second month’s auto-renewal; why some cards work for regular online purchases but cannot be linked to services like Netflix; and why a card may work on one platform but get rejected on another.

- For Stablecoin Users, the Real Hassle Is “Being Forced to Take Detours”

If platforms directly accepted USDT or USDC, users could complete payments with their on-chain balance. But in reality, most overseas subscription services still rely on card payments.

Thus, stablecoin users are funneled back into the traditional payment system: sell U, wait for settlement, link a card—or find a card that can be topped up with stablecoins. Any hiccup along the way leads to payment failure.

This is why “failed overseas subscription payments” are so closely tied to USDT’s daily spendability. It’s not purely a bank card problem—it’s the first conversion barrier stablecoin users encounter when trying to use on-chain assets for real-world digital services.

For AI freelancers, developers, Web3 creators, and remote workers, this issue is especially acute. ChatGPT, Claude, Codex, Midjourney, cloud services, ad accounts, and development tools are often part of daily workflows. When a tool’s subscription lapses, work is disrupted.

Daily Spending: You Have stablecoins, but Merchants Take Fiat—Leaving You with C2C Cash-Out First

Compared to overseas subscriptions, daily spending presents a more straightforward problem.

Many USDT holders think: since this is a stablecoin pegged to the dollar, can’t I use it directly for everyday purchases? You just want to buy an item online, pay a small order, or cover a routine expense—but instead, you have to sell U, wait for funds to arrive, confirm receipt, and then link a payment tool.

The reality is that most merchants don’t directly accept USDT. Whether they’re local businesses, online platforms, or common payment tools, settlement is almost always in RMB, USD, EUR, or another local fiat currency.

This creates the second barrier: you hold stablecoins, but spending scenarios accept fiat.

- How Many Steps Does It Take to Go from USDT to Daily Payment?

Without a stablecoin payment card or other bridging tool, users typically follow a traditional path to convert USDT into spendable funds.

The common flow is:

- Sell USDT on an exchange or C2C market;

- Wait for the buyer to pay or the platform to process;

- Fiat enters your bank account;

- Use a bank card, credit card, or local payment tool to spend.

This process seems workable, but it’s not suited for small, frequent, or ad-hoc daily purchases.

If you just want to pay for a dozen-dollar subscription or make an impromptu online purchase, you still have to sell U, wait for settlement, confirm receipt, and link a card—even though your assets are already sitting in your wallet.

- Why Does C2C Cash-Out Stress Out Many Users?

C2C cash-out is a common approach for stablecoin users, but it’s more like “turning U into spendable money” than a truly convenient way to pay for daily needs.

- Unpredictable timing.

C2C transactions depend on buyer-seller matching. Settlement speed, price, and counterparty reliability all affect the experience. When a payment is urgent, you can’t count on this path being fast enough.

- Opaque costs.

Selling USDT/USDC may involve bid-ask spreads that vary across platforms, times, and fiat channels. For small, frequent purchases, each individual loss seems minor, but over time, it meaningfully eats into your available funds.

- Bank account risk pressure.

Frequent C2C receipts can leave your bank account with multiple incoming transfers from various counterparties. For ordinary users, this pattern can sometimes trigger bank inquiries, limits, or other risk-control measures.

- Complex record-keeping.

Each sale, receipt, and subsequent spend generates a trail of transactions. For freelancers, remote workers, or stablecoin-receiving users, reconciling accounts over time becomes a real hassle.

- Daily Spending Needs a Shorter Payment Path

Most users don’t want to turn USDT into a complex financial operation. They simply wish the stablecoins they already hold could be used more conveniently for real purchases.

If every transaction requires “sell U → receive funds → deposit → link card → pay,” the utility of stablecoins is severely diminished.

So the pain point of USDT/USDC daily spending isn’t just whether merchants accept U directly—it’s also the lack of a stable, sustainable bridging tool suited for small, frequent transactions.

This is why U-cards are under discussion: they aim to connect stablecoin balances with card payment functionality, so users don’t have to start with C2C cash-out every single time.

Cross-Border Travel: Stablecoins Transfer Fast, but Spending Still Relies on Card Networks

USDT, USDC, and other stablecoins are naturally well-suited for cross-border transfers. They can move 24/7, independent of banking hours, without waiting for multiple intermediary layers as in traditional wire transfers.

Yet when it comes to actual spending, the problem reappears.

When traveling abroad, working remotely, shopping overseas, booking hotels, buying flights, or paying for international services, merchants overwhelmingly settle in local fiat via bank cards, credit cards, or card networks. Your stablecoins still need to enter the real-world payment channel.

- Stablecoins Can Cross Borders Quickly, But There Is Still Considerable Friction in the Final Consumption Process

Many Web3 users, digital nomads, or overseas freelancers hold their assets primarily in USDT, USDC, and similar forms. For them, stablecoins are highly convenient for cross-border income, remote collaboration, and on-chain transfers.

But when they actually need to spend, the path often becomes:

USDT / USDC → Sell for fiat → Withdraw to bank account → Spend abroad via card or currency exchange.

This dilutes the cross-border advantage of stablecoins at the very last step.

On-chain transfers can complete quickly, but real-world spending still goes through bank accounts, currency conversion, card networks, merchant acquiring, and risk-control systems. You seem to have a global asset, yet you’re still funneled back into traditional forex and card-swiping processes.

- The Cost of Cross-Border Spending Goes Beyond a Single Fee

Common costs in traditional cross-border spending include:

- Currency conversion fees;

- International transaction fees;

- ATM withdrawal fees;

- Foreign bank terminal fees;

- Exchange rate spreads;

- Additional rules from issuing banks or payment institutions;

- Risk controls triggered by out-of-region, nighttime, or atypical transactions.

If you sell U first, then spend cross-border through a domestic bank card or local account, you may go through multiple conversions:

stablecoin → local fiat → foreign currency → card network settlement. Each layer can introduce fees, waiting time, or risk-control uncertainty.

For occasional travelers, this might be merely inconvenient. For those working cross-border long-term, regularly subscribing to overseas services, or frequently moving between countries, it represents a persistent cost.

- Stablecoin Users Need “Spending-Side Connectivity”

Stablecoins solve the cross-border transfer problem, but they haven’t automatically solved the cross-border spending problem.

Whether users can actually spend their funds ultimately depends on what payment methods the spending end supports. Most real-world merchants don’t handle on-chain transfers directly—they’re accustomed to accepting bank cards, credit cards, Apple Pay, Google Pay, or local payment tools.

So for stablecoin users, cross-border spending isn’t just about whether the money can be moved—it’s also about whether that money can be accepted by merchants when paying at a store, booking a hotel, buying a ticket, or covering a subscription.

This is where stablecoin payment cards provide value: they don’t change how every merchant gets paid, but they make it easier for users’ stablecoin balances to access the already-mature card payment network.

In the exploration of this type of “stablecoin consumption infrastructure”, BenPay is one of the stablecoin payment products incubated by Bixin Group, dedicated to connecting on-chain assets with the real payment network.

U-Cards: Connecting USDT/USDC to the Card Payment Network and Shortening the Conversion Path

U-cards—also known as crypto payment cards or stablecoin payment cards—serve as a layer of connectivity between on-chain assets and real-world spending.

They typically don’t require merchants to accept USDT directly, nor do they turn every business into an on-chain merchant. More commonly, users top up the card with stablecoins like USDT or USDC and then spend via Visa/Mastercard networks in scenarios that accept card payments.

Simply put, U-cards do one thing: convert stablecoin balances into card payment capability that’s more readily accepted by the traditional payment system.

- The Core Problem U-Cards Solve

In the traditional path, stablecoin users often go through:

USDT → Sell → Fiat deposit → Bank card/Credit card → Spend.

U-cards aim to shorten this to:

USDT / USDC → Top up card → Pay with card.

The value is in reducing intermediate steps—especially the frequent need to cash out via C2C, wait for bank settlement, re-link payment tools, and handle multi-layer currency conversions.

For overseas subscriptions, cross-border spending, digital nomads, Web3 freelancers, and stablecoin-receiving users, this approach is far more aligned with daily habits.

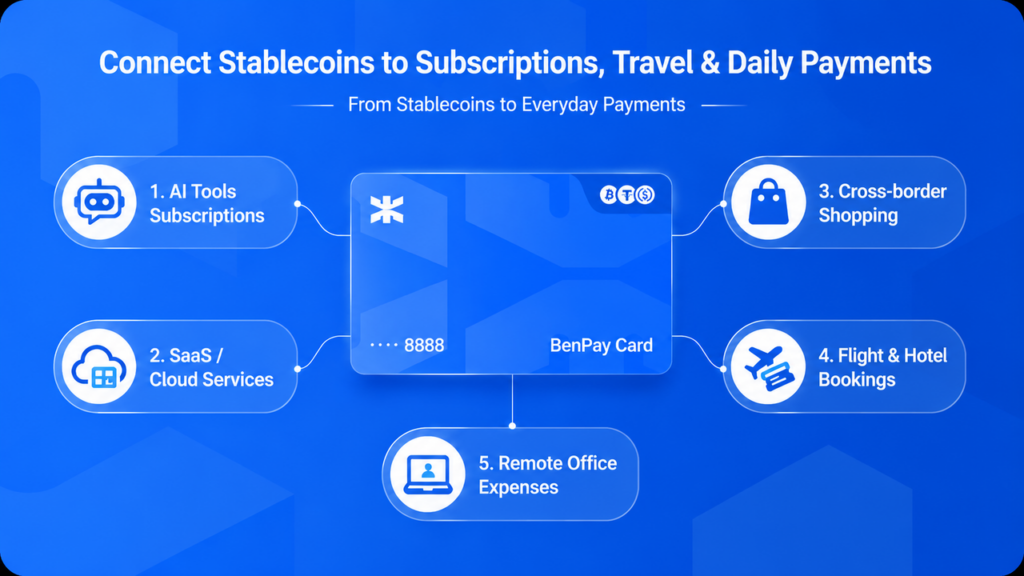

- Which Scenarios Can U-Cards Improve?

A stablecoin payment card typically helps users in the following scenarios:

- Overseas AI tool subscriptions like Codex, ChatGPT Plus, Claude, Midjourney, etc.

- Subscriptions for overseas SaaS, cloud services, ad accounts, developer tools, etc.

- Cross-border e-commerce shopping, travel expenses, hotel and flight bookings;

- Daily online spending for users who receive stablecoin income;

- Reducing the hassle of repeatedly selling U, withdrawing, converting currency, and re-linking cards;

- Spending in payment scenarios that support card linking.

It’s important to note that U-cards aren’t a universal solution. They still must comply with issuer policies, card network rules, merchant platform requirements, and local regulatory frameworks. Different cards vary in supported regions, KYC requirements, limits, fees, recurring billing capabilities, physical card availability, and ATM withdrawal functionality.

So when choosing a U-card, don’t just consider “whether I can get one”—assess whether it suits your specific spending needs.

- What Should You Look for When Choosing a U-Card?

For stablecoin users, key factors to evaluate include:

- Whether USDT/USDC top-ups are supported;

- Whether multi-chain top-ups are supported and the convenience of the funding path;

- Whether the card suits overseas subscriptions and cross-border spending;

- Whether it supports recurring billing and Card-on-File scenarios like long-term subscriptions;

- Whether there are issuance fees, top-up fees, transaction fees, monthly fees, or currency conversion fees;

- Whether physical cards, ATM withdrawals, or mobile wallet binding are supported;

- Whether KYC requirements, limits, and features match your needs;

- Whether issuer resources, fee structure, and usage restrictions are transparent;

- Whether prohibited uses and compliance boundaries are clearly stated.

In particular, avoid being swayed by claims like “no KYC,” “low-cost issuance,” or “instant activation and use.” For real spending, card stability, fee transparency, and scenario fit matter far more. Many U-cards on the market frequently face payment rejections after top-up. We’ve done an in-depth analysis of the underlying reasons in Why Crypto Card Payments Get Stuck — and How to Make USDT/USDC Spending Feel More Like Cash. We strongly recommend understanding the fundamental security differences between custodial and non-custodial models before getting a card.

How Can BenPay Card Improve the USDT Daily Spending Experience?

Among stablecoin payment cards, BenPay Card is designed for users who already hold USDT/USDC but want to reduce the hassle of selling U, withdrawing funds, converting currencies, and linking cards. Its value lies not in making every merchant accept stablecoins directly, but in enabling users to spend their stablecoin balances across more online subscriptions, cross-border purchases, and daily payment scenarios via the card payment network.

For existing USDT/USDC holders, BenPay Card offers a shorter path: top up the card with stablecoins and use it for online subscriptions, cross-border spending, and everyday payments where card payments are accepted.

- For Overseas AI Tools and SaaS Subscriptions

Many users turn to BenPay Card primarily for paying overseas AI tools and SaaS services—for example:

- ChatGPT Plus;

- Codex;

- Claude Pro;

- Midjourney;

- Overseas cloud services;

- Developer tools;

- Overseas ad platforms;

- Streaming and digital subscription services.

These platforms largely still depend on card payments. For stablecoin users, BenPay Card reduces the “sell U → deposit → link card” sequence, making subscription payments more streamlined.

However, whether a given overseas platform ultimately accepts the payment still depends on merchant policies, platform risk controls, account region, card status, and user behavior. No payment card can guarantee 100% success across every platform.

A more realistic understanding is that BenPay Card provides stablecoin users with a card payment path better suited for overseas subscription scenarios.

- For Cross-Border Spending and Remote Work Expenses

For digital nomads, Web3 freelancers, cross-border e-commerce operators, and remote workers, daily expenses are often spread across different countries and platforms—for example:

- Overseas software subscriptions;

- Cross-border e-commerce purchases;

- Hotel, flight, and transport bookings;

- Team collaboration tools;

- AI API or cloud service bills;

- Payments for overseas online services.

If your income or primary assets are already in USDT/USDC, cashing out to a bank account before every cross-border payment makes the process very heavy.

BenPay Card integrates stablecoin top-up and card spending into a single path, reducing the repeated back-and-forth of currency conversion, withdrawals, and re-linking payment tools.

- Multiple Card Types for Different Needs

Not all users have the same requirements for a U-card. Some need occasional overseas subscription payments, others need higher spending limits, and still others prioritize physical cards, ATM access, or more comprehensive functionality.

BenPay Card offers different card options to suit varied needs:

- Alpha Card: suited for light online payments and lower-threshold usage;

- Sigma Card: designed for more cross-border spending and broader card usage scenarios;

- Delta Card: suited for higher limits, physical card, or more feature-rich requirements.

Different cards may vary in fees, limits, KYC requirements, available features, and applicable scenarios. Users should refer to the official BenPay page for current information before choosing.

- What Should You Keep in Mind When Using the BenPay Card?

BenPay Card is a stablecoin spending tool. Users should be aware that:

- Platform acceptance of card payments varies;

- Available scenarios are subject to merchant rules and payment network policies;

- KYC, limits, fees, and features are subject to official updates;

- Successful overseas subscriptions still depend on platform risk controls;

- Stablecoin top-up and spending records should be managed responsibly;

- Applicable local laws, regulations, and platform terms of service must be observed.

From a positioning standpoint, BenPay Card is best suited for users who already hold stablecoins and want to reduce the steps of C2C cash-out, bank deposit, currency conversion, and re-linking cards.

It offers not a “bypass all restrictions” solution, but a shorter and clearer spending path for stablecoins.

Final Thoughts: Stablecoins Need Better Bridging Tools to Enter Daily Spending

USDT, USDC, and other stablecoins have become essential tools for cross-border payments, remote collaboration, and on-chain asset management. Yet in real-world spending, users still encounter numerous friction points.

Overseas subscription platforms don’t directly accept U—users are funneled back into the card system. Daily spending scenarios require fiat—users have to cash out first. And during cross-border travel or remote work, stablecoins’ global liquidity advantage is often undercut by currency conversion, risk controls, and traditional card payment processes.

Behind all these challenges lies a single need: users don’t just need to hold stablecoins—they need a payment gateway that lets them spend them.

U-cards and crypto payment cards have emerged precisely to fill this gap. They don’t bring every merchant onto the blockchain; instead, they connect stablecoin balances to the mature card payment network that already exists, allowing users to spend on-chain assets in more card-accepting scenarios.

For those already holding USDT or USDC, a stablecoin payment card like BenPay Card represents a option worth considering. It reduces the friction of switching between selling U, withdrawing, converting currencies, and linking cards—bringing on-chain assets closer to daily spending.

If stablecoins solved the “global transfer” problem, stablecoin payment cards are tackling a more practical one: how to make on-chain assets actually enter everyday payment scenarios.

U-Card FAQ

Q: Why does my ChatGPT Plus payment fail?

A: Common reasons include domestic credit cards being blocked by issuing banks, virtual card BINs flagged as high-risk or prepaid, or the card not supporting stable recurring billing (Card-on-File). You can try a card type better suited for overseas subscriptions and recurring billing, but the actual outcome still depends on platform risk controls and account status.

Q: What fees are involved with a U-card?

A: Fees vary across products but commonly include issuance fees, monthly/annual fees, transaction fees, and currency conversion fees. It’s best to choose a product with transparent fees that fits your cross-border and subscription scenarios, and to verify the latest rules before use.

Q: Is a U-card safe? Will it be frozen?

A: U-cards issued by properly licensed institutions generally have clearer fund flows, but transaction restrictions may still occur based on issuer policies, merchant platforms, user behavior, KYC status, and local compliance requirements. With normal compliant usage, risks are relatively manageable.

Q: Can I get a U-card without KYC?

A: Some U-cards offer simplified sign-up options (e.g., requiring only a phone number or email) suitable for privacy-conscious light users; higher-limit or full-feature cards typically require KYC. Specifics are subject to official rules.

Q: Can a U-card be used for overseas ATM withdrawals?

A: Versions supporting physical cards usually allow ATM withdrawals in many countries and regions, though specific coverage and fees are subject to official information.

Q: What’s the difference between a U-card and a regular credit card?

A: Regular credit cards draw on bank credit or fiat deposits; U-cards are funded by stablecoin balances like USDT and USDC that users top up to the card. This removes some of the “sell U → withdraw → link card” steps, making stablecoin spending more direct—though card network rules still apply.