Introduction

It is late at night. You have just landed a $3,000 AI fine-tuning project on Upwork. You open Notion to update your schedule and, almost at the same time, try to renew your Claude API subscription. Then your bank card gets declined again.

You pull out your USDT and consider converting it into fiat, only to find that the C2C exchange rate has gone up by another two points. In the end, you open Excel and start calculating: you earned $8,000 this month, but nearly $100 has already been eaten up by transaction fees, exchange rate losses, and payment friction.

This is not an isolated case. It is becoming part of the everyday reality for AI freelancers in 2026.

In 2026, AI prompt engineering, model fine-tuning, AI content generation, and AI agent services are becoming some of the fastest-growing categories in the global freelance market. According to Upwork’s 2026 In-Demand Skills Report, demand for AI-related skills increased by 109% year over year, while demand for AI video generation and editing grew by as much as 329%.

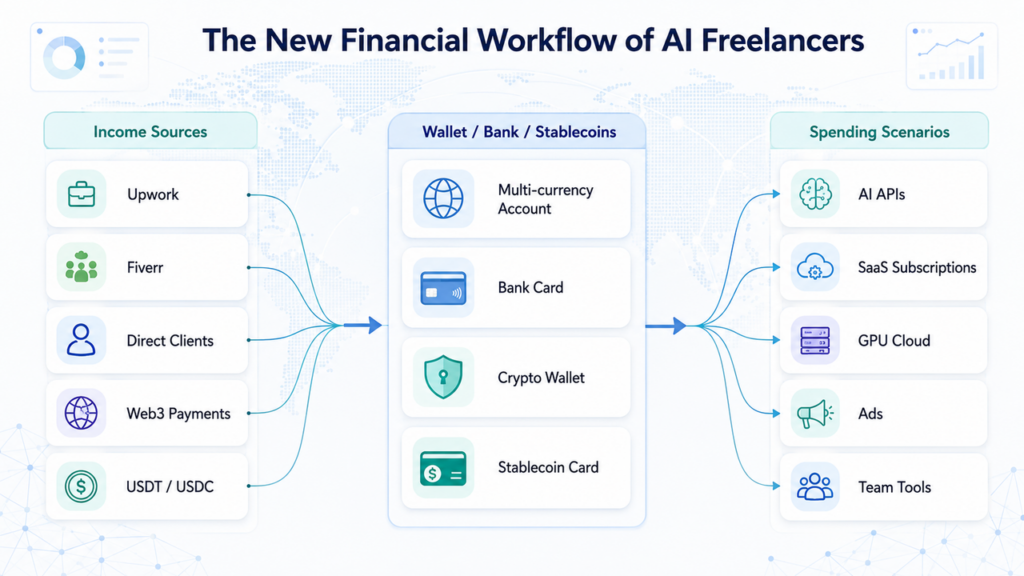

As AI commercialization accelerates, more AI freelancers are earning global income through Upwork, Fiverr, remote collaboration platforms, and direct enterprise contracts. At the same time, their expenses are becoming increasingly global as well, covering OpenAI API, Anthropic and Claude, Midjourney, GPU cloud services, overseas advertising, and global SaaS tools.

This means the financial workflow of AI freelancers has shifted from the traditional model of “local income and local spending” to a new digital work model built around “global income, global spending, and multi-currency collaboration.”

However, the traditional cross-border financial system still comes with slow settlement, high transaction fees, exchange rate losses, payment restrictions, and complex tax management. For AI freelancers, the ability to earn globally, spend globally, and manage money globally is becoming a core factor that affects long-term growth.

This article will break down an integrated revenue and expenditure management solution for AI freelancers, combining real-world examples and industry trends to provide practical, actionable suggestions.

Core Pain Points and Needs of AI Freelancers

In a globalized and digital-first work model, more freelancers are facing new challenges in payments and financial management. A typical digital creator or remote worker may now have a daily workflow that includes:

- Taking international projects through Upwork and Fiverr

- Maintaining long-term subscriptions to professional tools and services

- Renting cloud servers and computing resources

- Acquiring clients through channels such as Google Ads and LinkedIn Ads

- Collaborating through SaaS tools such as Notion, Figma, and Canva

- Receiving part of their overseas income in stablecoins such as USDT and USDC

Their income comes from around the world, and their expenses also flow across borders. However, the traditional financial system was not designed for this model of “global income plus high-frequency global spending.”

As a result, the following core pain points continue to affect AI freelancers:

- High Costs from Multi-Currency Conversion and Hidden FX Fees

Many AI freelancers earn their income in U.S. dollars, but their daily expenses, living costs, and local bank card systems still operate in local currencies.

For example, an AI video creator may receive USD income from Upwork, withdraw it to a local bank account, and then use a local credit card to pay for OpenAI API, Midjourney, Google Ads, and other global services. During this process, the money may go through multiple currency conversions and foreign exchange markups.

With long-term and high-frequency subscriptions, these hidden costs can add up to tens or even hundreds of dollars per month.

Traditional bank card systems are mainly built around local fiat currencies. Cross-border payments still depend heavily on banking settlement networks, making it difficult to truly optimize multi-currency cash flow for global digital workers.

- Unstable Payments for Overseas AI Tools

Many AI freelancers have experienced a common problem: the card works locally, but fails when paying for overseas services.

For example, an AI agent developer may have an OpenAI API payment declined during an automatic nighttime charge because the transaction triggers bank risk controls. As a result, the API service is interrupted and the client’s workflow is affected.

Overseas SaaS services such as ChatGPT Plus, Claude Pro, Cursor, and Midjourney often involve payment failures, risk-control blocks, and interrupted auto-renewals.

Traditional bank risk-control systems are better suited to offline consumption and local transaction patterns. However, payments for AI tools are often high-frequency, small-value, automated, and cross-border. This makes them more likely to be misclassified as abnormal transactions.

- Fast-Growing Demand for AI Agent Automated Payments

As AI agents begin to handle procurement, ad spending, API calls, and service settlement on their own, programmable, high-frequency, instant, and small-value payments are becoming increasingly important.

For example, an automated marketing agent may increase a Google Ads budget based on campaign performance, or automatically renew GPU computing resources when capacity is running low.

If every payment step requires manual confirmation, the efficiency of automation is immediately reduced.

Traditional bank card systems assume that the payment initiator is a human user. They are not well suited for AI agents that need to initiate frequent transactions autonomously. As a result, they struggle to meet the new payment needs of the AI automation era.

- A Serious Gap Between On-Chain Assets and Real-World Spending

More AI teams are using stablecoins such as USDT and USDC to receive income. However, they still face a frustrating reality: on-chain assets are easy to receive, but difficult to spend in real life.

Common problems include:

- Stablecoins cannot be used directly to subscribe to overseas SaaS services.

- Users often need to withdraw or convert assets into a bank card before spending.

- Each conversion may create additional fees, delays, FX losses, and more complex tax records.

For example, an AI plugin developer may hold a large amount of USDC in a wallet, but still cannot directly pay for ChatGPT Plus, AWS, Figma, or other global services. The developer has to withdraw funds, convert currencies, and re-enter the traditional payment system before making the payment.

This process not only increases fees and time costs, but also weakens the key advantages of stablecoins: low-cost transfers and instant settlement.

The long-standing lack of a native connection between traditional finance and on-chain assets means that stablecoins are still difficult to integrate directly into mainstream spending scenarios.

- Low Efficiency in Global Financial Management

For many AI freelancers and small AI teams, financial management is becoming increasingly fragmented.

Income may be spread across Upwork, Fiverr, direct enterprise contracts, and crypto wallets. Expenses may be scattered across different bank cards, virtual cards, and crypto wallets.

This creates several problems:

- Bookkeeping becomes difficult.

- Invoice management becomes more complicated.

- VAT, GST, and cross-border tax processing become more costly.

- Cash flow becomes harder to track in real time.

For example, in a small AI studio, a designer may pay for Figma with one card, a developer may pay for GPU resources with USDT, and the founder may manage advertising expenses separately. At the end of the month, the team may still need to rely on Excel for manual reconciliation.

Traditional bank card systems are mainly designed around personal spending or conventional business finance. They are not built for the financial needs of AI teams that operate globally, combine on-chain and off-chain assets, and collaborate across multiple platforms.

AI freelancers are no longer facing a single “cross-border payment” problem. Instead, they are dealing with a broader financial challenge that includes multi-currency management, payment stability, AI agent automation, stablecoin spending, and tax coordination.

Comparison of Mainstream Cross-Border Payment Platforms in 2025–2026

As AI freelancers face increasingly complex global income and spending needs, the market has already seen the rise of various cross-border payment and fintech solutions.

Different platforms have different strengths when it comes to payment collection, currency conversion costs, spending convenience, automation support, stablecoin compatibility, and adaptability to AI agent payments.

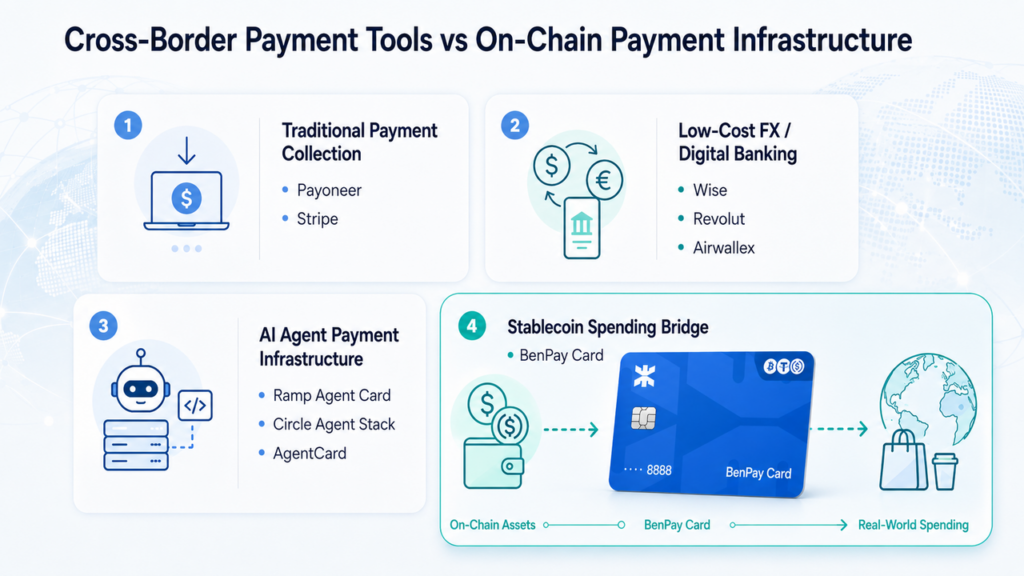

From traditional cross-border payment platforms to digital banks, and from fintech cards to next-generation on-chain payment infrastructure built for AI agents and stablecoins, the entire industry is gradually evolving from simple “cross-border payment tools” into a broader “global financial operating system.”

The following comparison is based on common use cases and publicly available platform positioning. Fees, availability, and account requirements may vary by region and user type.

| Platform | Best Use Case | Core Advantages for AI and Cross-Border Work | Key Limitations and Pain Points | Account Requirements and Barriers | Fee and Cost Profile |

| Airwallex | Overseas ad spending and AI Studio operations | A full-stack financial operating system with strong support for bulk virtual cards and employee expense management. Well suited for large-scale advertising campaigns and high-frequency API billing. | Does not support crypto assets. Risk controls may be sensitive to small-value, high-frequency retry transactions. | High barrier: usually requires a domestic or overseas business license. | Close to interbank exchange rates, with very low FX markup. |

| Payoneer | Freelancers taking projects from traditional global platforms such as Upwork and Fiverr | Strong platform integration. Smoothly connects with major freelance marketplaces, supports automatic payouts, and provides mature multi-currency receiving accounts. | Fee structure is relatively traditional and lacks automated financial or expense collaboration features. | Low barrier: available to individuals and small studios. | Overall conversion and withdrawal fees are relatively high, often around 1.2%. |

| Wise Business | Lightweight global transfers and low-cost currency conversion | One of the most cost-effective options for currency exchange. Uses the mid-market exchange rate, offers low conversion losses for large cross-border transfers, and supports flexible fund movement. | Virtual card risk controls can be strict and may trigger additional verification when IP locations change frequently. | Medium barrier: supports individual applications, but address verification for mainland China users has become stricter. | Excellent exchange rates with transparent and low fixed fees. |

| Revolut Business | Digital nomads and settlement with European or UK clients | A strong digital banking experience with smooth multi-currency account switching, fast local clearing networks in Europe, and a UI/UX that fits internet-native users. | Localized support and withdrawal channels in Asia, including mainland China, may be limited. | High barrier: usually requires a European or UK company entity or overseas identity documentation. | Basic plans may be free, while advanced features usually follow a monthly subscription model. |

| Stripe | Global online payment collection for AI SaaS and digital products | A leading global payment infrastructure provider. Its developer-friendly APIs make it a preferred option for AI products that need subscriptions, one-time payments, or token-based billing models. | It is a payment acceptance interface rather than a spending card, so it must be combined with other bank cards or financial tools to create a complete payment loop. | Medium to high barrier: requires compliant merchant qualifications, with Stripe Atlas available for overseas company setup. | Charges a percentage-based fee per transaction, commonly around 2.9% + $0.30. |

| Ramp Agent Card | AI agent automated spending and enterprise AI tool procurement | An enterprise-grade payment system designed for AI agents, supporting automated payment permissions, API usage management, and SaaS expense control. | Mainly serves the U.S. enterprise ecosystem and is not very friendly to individual users. | High barrier: usually requires a U.S. company entity. | Enterprise subscription model, with some features charged on a per-seat basis. |

| Circle Agent Stack | Stablecoin settlement and on-chain AI agent payments | Natively supports USDC and on-chain automated settlement, enabling AI agents to receive and make payments autonomously and move funds on-chain. | More like developer infrastructure than a consumer-facing product, so the entry barrier is relatively high for ordinary users. | Developer- and enterprise-oriented, requiring technical integration capabilities. | On-chain settlement costs are low, but they may fluctuate depending on network gas fees. |

| AgentCard | AI agent-native spending and stablecoin payments | Focuses on enabling AI agents to directly access payment capabilities, with support for stablecoins and automated spending scenarios. | The ecosystem is still at an early stage, with limited merchant coverage and payment network reach. | Medium barrier: more suitable for Web3 users and developers. | Lower on-chain payment costs, making it suitable for high-frequency micropayment scenarios. |

It is clear that as AI freelancers and the AI agent economy continue to grow rapidly, traditional cross-border payment platforms can already solve part of the payment collection and currency conversion problem. However, most systems remain fragmented.

Some platforms are better suited for receiving payments. Some focus on currency conversion. Others are more designed for enterprise expense management and financial collaboration. Meanwhile, next-generation agent payment platforms such as AgentCard and Circle Agent Stack are beginning to build around AI automated payments and on-chain fund flows.

This shift is especially important in areas such as stablecoin settlement, AI tool subscriptions, high-frequency API payments, and Web3 asset movement. Traditional fintech infrastructure is gradually becoming less capable of meeting the new payment needs of the AI era.

At the same time, the payment system itself is changing. In the past, payment networks mainly served human users. In the future, payment networks may also need to serve AI agents, automated workflows, and machine-to-machine financial collaboration.

But for most AI freelancers, digital creators, and Web3 users, the more practical question remains: how can on-chain assets be used for real-world global spending and everyday payments?

Compared with agent payment platforms that focus more on AI automation infrastructure, a new generation of crypto payment cards acts as a more practical bridge between stablecoin assets and real-world payment networks.

BenPay Card is one representative product in this direction.

A Next-Generation On-Chain Payment Solution for AI Freelancers: BenPay Card

BenPay Card is not just a regular crypto payment card. It is an on-chain payment tool designed for stablecoin users, digital nomads, and global freelancers.

It helps users turn their work income directly into global spending power, simplifying the entire financial workflow of earning globally and spending globally.

- Spend On-Chain Assets Directly Without Repeated Withdrawals

A traditional payment process usually involves several steps: after receiving USDT, the user needs to convert it into fiat through C2C platforms or exchanges, transfer the funds to a bank card, and then use that card to subscribe to overseas services.

This process creates multiple layers of transaction fees, FX losses, delays, and even the risk of account freezes.

BenPay Card supports multiple major blockchains, including Ethereum, Solana, Tron, BSC, Polygon, and Arbitrum, while also optimizing gas costs. Users can top up their card directly with stablecoins and spend globally through the Visa and Mastercard payment networks.

This makes it easier to pay for overseas subscriptions, cloud services, advertising campaigns, and SaaS tools without repeatedly withdrawing, converting, and moving funds across different systems.

- Self-Custody and On-Chain Transparency: Users Stay in Control

BenPay Card follows a decentralized self-custody model. Unlike some centralized platforms, it gives users more control over their funds.

- User assets are managed through smart contracts.

- Fund flows are transparent, traceable, and verifiable on-chain.

- Users can freeze or unfreeze their cards directly in the app at any time.

This allows users to keep real control over their funds, improving both security and autonomy.

- Different Card Types for Different Stages of Growth

BenPay Card offers three card options based on different user needs and usage stages:

- Delta Card, recommended for individual creators: With a low entry barrier, Delta is suitable for individual freelancers and digital nomads. It is designed to support long-term subscriptions to mainstream global tools.

- Sigma Card, recommended for high-frequency payments: Sigma is optimized for frequent small-value payment scenarios. It can help reduce transaction costs and payment failure rates, making it suitable for automated tasks and recurring spending.

- Alpha Card, recommended for teams and studios: Alpha provides higher limits, multi-card management, and support for larger payments. It is better suited for users who have moved into small-team collaboration or studio-level operations.

How BenPay Card Solves Payment Problems for Global Freelancers

| Core Pain Point | BenPay Card Solution |

| Repeated withdrawals and high currency conversion costs | Supports direct stablecoin top-ups and spending, reducing unnecessary conversion steps. |

| High failure rates when paying for overseas subscriptions | Designed for overseas AI subscriptions and optimized for cross-border payment scenarios. |

| Limited support for automated payments | Offers different card types to fit high-frequency, small-value, and global payment needs. |

| Fragmented funds and complex financial management | Supports unified on-chain asset management and improves fund flow efficiency. |

With BenPay Card, freelancers can create a smoother connection between stablecoin income and global spending scenarios, reducing overall costs while improving the efficiency of fund usage.

Conclusion

As AI and global remote collaboration continue to develop, the way freelancers work is shifting from “local income and local spending” to a new stage of “global income, global spending, and multi-currency collaboration.”

For AI freelancers, the real challenge is no longer just cross-border payment collection. It now includes a full set of digital finance needs, such as global spending, stablecoin settlement, AI tool subscriptions, tax management, and fund coordination.

From traditional fintech platforms such as Airwallex, Payoneer, and Wise to next-generation on-chain payment solutions such as BenPay Card, the global payment system is moving toward a more digital, globalized, and integrated future.

As demand for stablecoin payments and AI agent payments continues to grow, future payment tools will no longer be just “payment tools.” They will gradually evolve into a new form of digital financial infrastructure that connects AI, on-chain assets, and global spending scenarios.

Q&A: Common Payment Questions for AI Freelancers

Q1: Why do many AI tools often experience payment failures?

Traditional bank card risk-control systems were not designed for high-frequency, cross-border, automated billing scenarios commonly seen in AI tools.

Overseas platforms such as OpenAI, Claude, Midjourney, and Google Ads may often trigger risk-control factors such as:

- A mismatch between the user’s IP location and the card issuing region

- High-frequency small-value automatic charges

- Continuous API calls during nighttime hours

- Long-term overseas SaaS subscriptions

- Previous risk-control labels associated with virtual cards

As a result, many AI freelancers have experienced problems such as:

- ChatGPT Plus renewal failures

- Claude Pro payment declines

- Automatic API suspension

- Abnormal payment issues in advertising accounts

At its core, this is a mismatch between the traditional bank card system and AI-native workflows.

Q2: Why are AI freelancers becoming more dependent on stablecoins?

Stablecoins are one of the most efficient and accessible digital dollar systems for global transfers today.

Compared with traditional cross-border bank transfers, stablecoins such as USDT and USDC offer several advantages:

- Faster settlement

- No dependency on banking hours

- Lower cross-border costs

- Better suitability for remote collaboration

- Better compatibility with Web3 payment collection

For AI developers, independent creators, and digital nomads, stablecoins are gradually becoming one of the default settlement methods for global collaboration.

Q3: Why is real-world spending still difficult after receiving stablecoins?

Most real-world spending scenarios still operate on traditional bank card networks.

Even after users receive income in USDT or USDC, they often still need to go through several steps:

- Withdrawal

- C2C currency conversion

- Bank card funding

- Binding the card to overseas payment platforms

This process is not only complicated, but also creates additional problems, including:

- FX losses

- Transaction fees

- Settlement delays

- Higher risk-control probability

- More complex tax records

This is why more users are beginning to pay attention to payment solutions that support direct stablecoin spending.

Q4: Why will AI agents change the future payment system?

AI agents are beginning to gain the ability to spend money autonomously.

In the future, more AI agents may automatically handle tasks such as:

- API procurement

- SaaS renewals

- Advertising budget allocation

- GPU computing rental

- Automated workflow collaboration

This means payment systems need to support high-frequency, small-value, automated, programmable, and globally instant settlement.

However, the traditional bank card system was originally designed around manual payments by human users. This makes it difficult to fully adapt to the AI agent era.

Q5: Who is BenPay Card best suited for?

BenPay Card is more suitable for users who have long-term needs around global income and global spending, such as:

- AI freelancers

- Digital nomads

- Web3 creators

- Users who receive income in stablecoins

- AI Studio teams

- Users with frequent overseas SaaS subscriptions

- Developers who regularly use OpenAI, Claude, GPU cloud services, and other global tools

Compared with the traditional process of “receive payment, withdraw, convert currencies, and then spend,” BenPay Card is designed to directly connect on-chain assets with global spending scenarios.

It helps users reduce unnecessary intermediate steps and lower the overall cost of moving and using funds.

Risk Disclaimer

This article is for informational and educational purposes only and does not constitute investment advice, financial advice, or a product recommendation.

The use of any cross-border payment service, virtual card, or stablecoin-related service may involve potential risks. Users should conduct their own risk assessment and take appropriate security measures.

Before using any related service, users should conduct independent research and, where necessary, consult professional advisors. The author and this article shall not be held responsible for any losses arising from the use of the information provided in this article.