Introduction: The 2026 World Cup — A Cross-Border Spending Challenge Across Three Currencies

The 2026 FIFA World Cup will be the largest tournament in the history of the competition, and the first ever to be jointly hosted by the United States, Canada, and Mexico. For football fans, it will be a global celebration of the sport. But for travelers, it also represents a complex cross-border spending journey across three different currency systems: USD, CAD, and MXN.

If you are planning to attend the World Cup, the real impact on your budget will likely go far beyond ticket prices. Hidden costs accumulate across multiple layers, including exchange rate fluctuations that distort budgeting, spread losses from repeated currency conversions, international card transaction fees, dynamic currency conversion (DCC) markups, and ATM withdrawal charges.

Individually, these costs may seem small or invisible. However, throughout a multi-country trip, they compound continuously and can significantly increase overall travel expenses.

This article breaks down the real cost structure of cross-border spending in the context of the 2026 World Cup, and explains why more travelers are turning their attention to stablecoin payments and next-generation payment card systems.

Why Does the World Cup Travel Amplify Cross-Border Payment Challenges?

The 2026 FIFA World Cup will be the first in history to span three countries— the United States, Canada, and Mexico. With 48 national teams, 104 matches, and 16 host cities, it will create the largest global human mobility event ever concentrated in a short period of time.

From a payments infrastructure perspective, this means millions of users will be making frequent transactions across countries, currencies, and merchants within a very short timeframe.

Typical spending scenarios include:

- Flight bookings

- Hotel accommodations

- Transportation

- Dining

- Shopping and entertainment

However, as more fans begin planning their budgets, a practical reality starts to emerge: World Cup tickets may not actually be the most expensive part of the trip. What is often underestimated is the cumulative cost of the entire cross-border spending system.

How Is Your Travel Budget Being “Silently Eroded”?

- Inflation: The Hidden Variable That Defines the “Price Baseline”

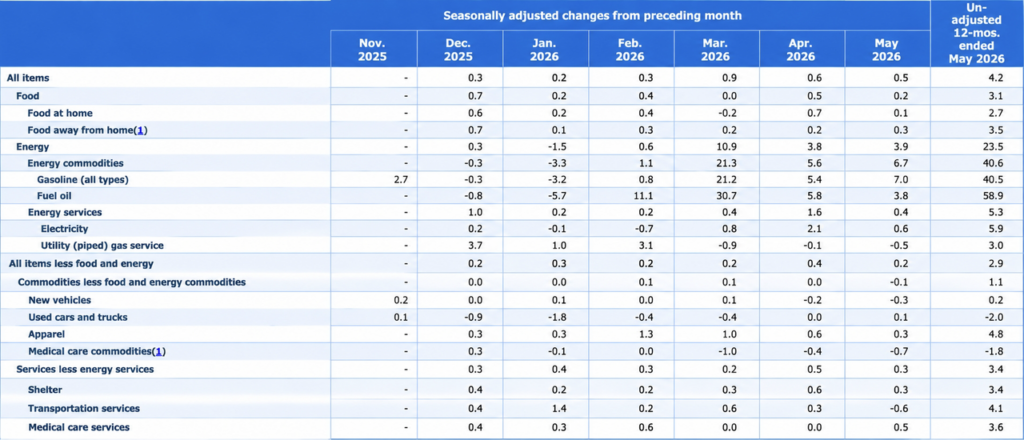

In the past two years, major global economies have broadly entered a “new normal after high inflation.” While the extreme inflation phase has passed, price levels have not meaningfully declined; instead, they have stabilized at a structurally higher range. Taking the latest U.S. data released on June 10 (BLS data) as an example:

- CPI increased 4.2% year-over-year

- Energy prices increased 23.5%

- Gasoline prices surged over 40%+

- Food and housing costs continued to rise

From a macro perspective, these figures do not necessarily indicate “runaway inflation.” However, from a consumer standpoint, the impact is very direct: the same budget today buys fewer services than before. This is not a short-term fluctuation, but a longer-term upward shift in the price baseline.

For travelers planning to attend the 2026 World Cup, this effect becomes even more pronounced due to the structural nature of travel consumption:

- Hotel prices surge during the tournament period

- Transportation and intercity mobility costs increase

- Dining and service-related expenses rise overall

- High-demand host cities experience severe price premiums due to supply-demand imbalance

Therefore, inflation does not act as a single isolated cost item. Instead, it uniformly raises the baseline of nearly all spending categories. In other words, inflation is not an “extra travel expense”—it is a shift in the underlying cost structure itself.

However, it is important to note that inflation is not the core issue in cross-border payments. It explains why things are getting more expensive, not why payments are becoming more complex. The real complexity comes from the next layer of variables—exchange rates.

- Exchange Rates: The Heavily Underestimated “Second Layer of Cost”

If inflation defines the “price level,” then exchange rates determine a far more practical question: how much you ultimately pay in your home currency.

The uniqueness of the 2026 World Cup lies in the fact that it spans three currency systems for the first time:

- USD (US Dollar)

- CAD (Canadian Dollar)

- MXN (Mexican Peso)

For travelers outside North America, the payment journey is rarely a single conversion. Instead, it becomes a multi-step chain: Home currency → USD → CAD / MXN → USD (settlement loop).

Under this structure, FX losses are no longer a “one-time conversion fee.” They become a continuously occurring, compounding cost chain.

Example FX Flow: How Many Conversions Does a World Cup Trip Actually Require?

Imagine a fan from Asia (starting from Tokyo) planning to attend the 2026 World Cup, traveling through Los Angeles, Toronto, and Mexico City before returning to Tokyo. In this journey, the flow of funds is not simply “spending USD abroad,” but a continuous reconstruction of currency exposure across different systems.

Before departure, the traveler typically converts JPY into USD (JPY → USD), since USD is the primary settlement currency for most international payments, flight bookings, and hotel reservations. Once arriving in the United States, if the journey continues to Canada, most expenses will be priced in CAD, requiring another conversion from USD to CAD (USD → CAD).

After moving from Canada to Mexico, the payment currency changes again, requiring funds to be converted into Mexican pesos (CAD → MXN or USD → MXN). Finally, at the end of the trip, any unused balance or remaining funds in the card may need to be converted back into JPY, triggering a reverse conversion (MXN → USD → JPY).

In total, across this complete World Cup travel route, the money effectively goes through a full multi-currency loop: JPY → USD → CAD → USD → MXN → USD → JPY — at least six currency conversions in total.

The key issue is that none of these conversions are “lossless.”

Even under relatively favorable conditions, each FX conversion typically incurs a 1%–2% spread or fee. When compounded across multiple conversions within a short period, the total accumulated loss can become significantly amplified. For a trip budgeted at around $5,000, hidden FX-related costs alone can easily reach 5%–10% or even higher.

In other words, what truly impacts the World Cup cross-border spending experience is not the price level of any single country, but the structural friction created by constantly switching between currencies.

- Cross-Border Payments: The Third Layer of Hidden Costs Beneath the Bill

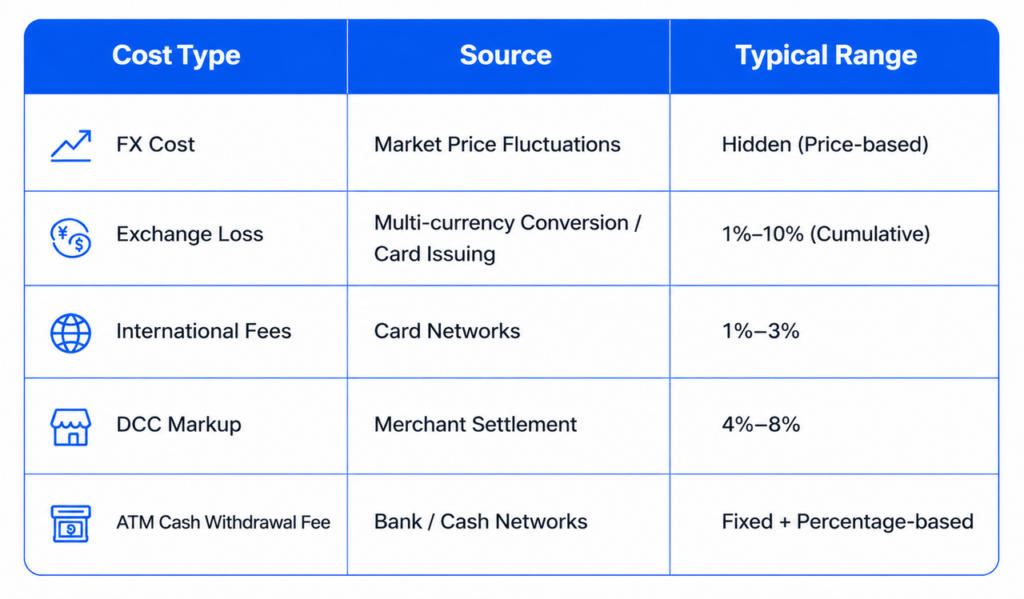

Beyond inflation and exchange rates, there is another cost structure that is even harder for users to directly perceive: the underlying processing fees embedded within payment networks. These costs are not shown as separate line items, but are instead distributed across every step of the transaction flow.

A typical cross-border payment passes through multiple layers: issuing bank → card network (Visa/Mastercard) → acquiring bank → FX clearing network → merchant. At each layer, fees or exchange rate adjustments may be applied.

Breakdown of Key Cost Sources:

- International Transaction Fees (1%–3%)

Charged by issuing banks or payment providers:

- Calculated as a percentage of the transaction amount

- Automatically triggered for overseas spending

- Accumulates significantly in high-frequency spending scenarios

- Dynamic Currency Conversion (DCC) (4%–8%)

This is one of the most common hidden premium sources in cross-border spending. When merchants ask: “Would you like to pay in your home currency?” it appears to be a convenience feature, but in reality it usually means:

- A non-optimal exchange rate is applied

- Additional conversion fees are embedded

- The final rate is significantly worse than market benchmarks

As a result, DCC is often one of the most overlooked but costly components of travel spending.

- FX Spreads + Settlement Costs (Hidden)

Even when no explicit fee is charged, several hidden cost components still exist:

- Bank bid-ask spreads

- Card network FX rate adjustments

- Cross-border settlement network fees

- Intermediary bank processing costs

These costs are typically bundled into the final exchange rate, making them difficult for users to identify directly—though they are always present in the pricing structure.

Summary of Cross-Border Payment Costs for the World Cup

The costs outlined above are not unique to the World Cup period. They are persistent across international travel, cross-border work, overseas study, and global consumer spending scenarios. As more users begin seeking more efficient ways to manage cross-border funds, stablecoin payments are increasingly coming into the mainstream.

Why Are More and More People Paying Attention to Stablecoin Payments?

It is precisely in the context of rising living costs driven by inflation, increased budget uncertainty caused by exchange rate volatility, and the long-standing inefficiencies and fees in traditional cross-border payment systems that more cross-border consumers are beginning to seek new ways to manage funds and make payments.

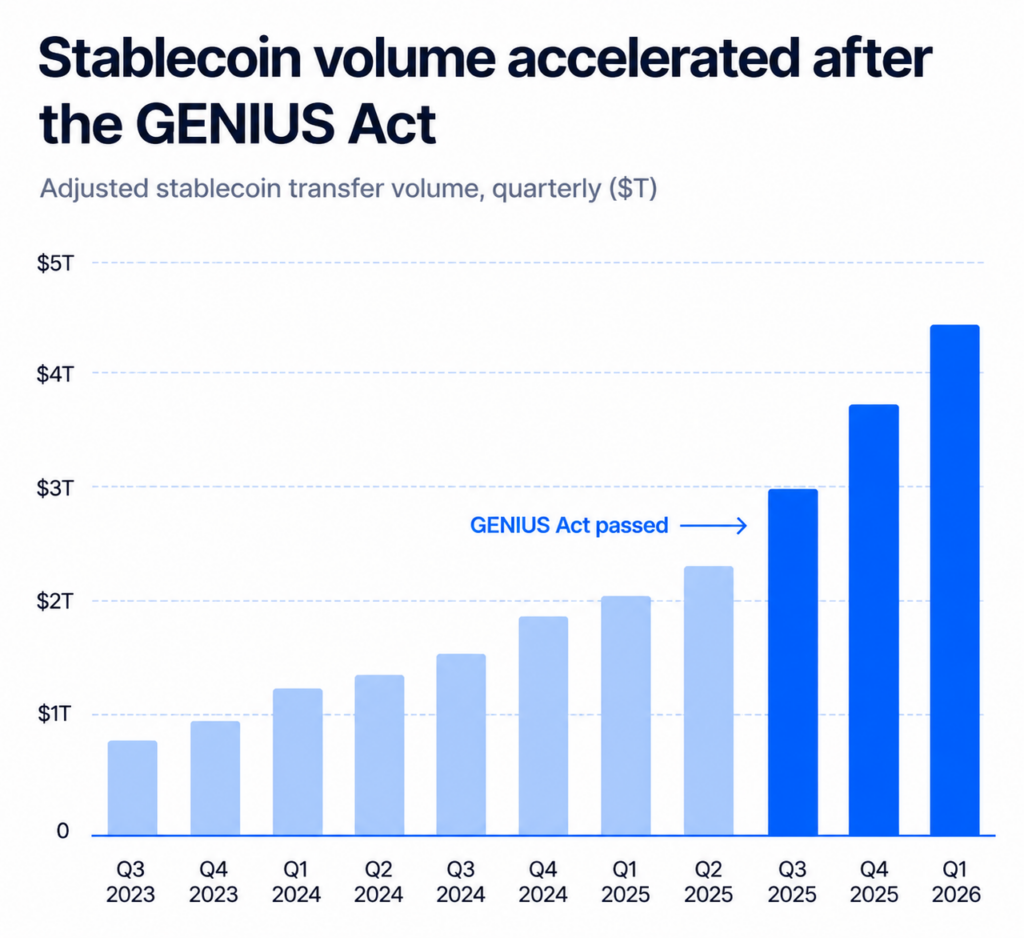

The 2026 cross-border consumption market is undergoing an unprecedented paradigm shift: regulated stablecoins such as USDT (Tether) and USDC (Circle) are rapidly evolving from crypto trading assets into everyday cross-border payment tools for global consumers.

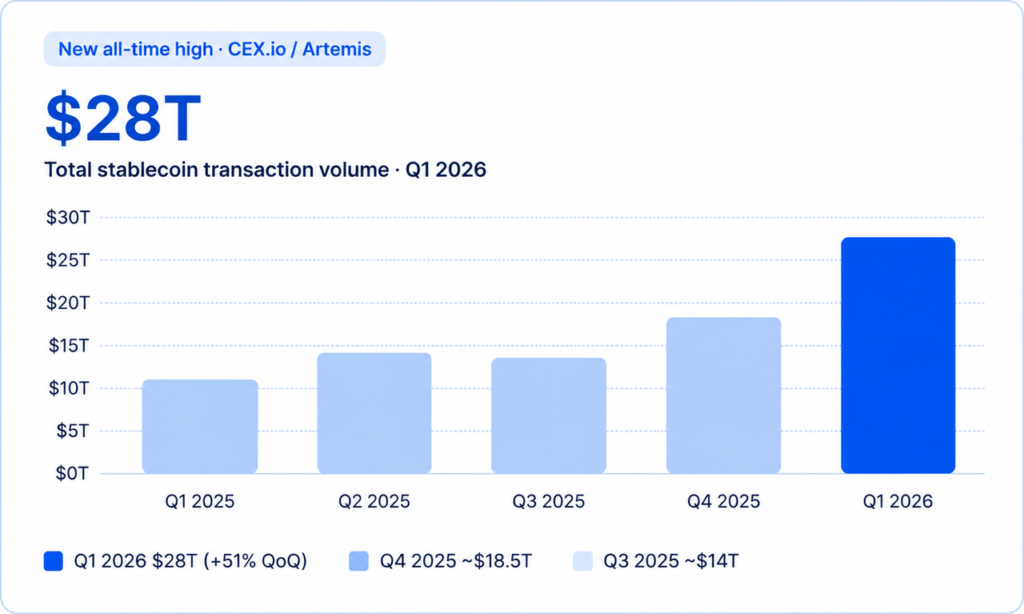

According to Stablecoins in Q1 2026, a report published by CEX.IO Research, global stablecoin on-chain transaction volume exceeded $28 trillion in Q1 2026. Meanwhile, adjusted transaction data from Artemis shows that after excluding internal transfers, arbitrage activity, and non-economic transactions, the volume of real economic activity involving stablecoins is approximately $4.5 trillion.

These figures reflect not only the growth of the crypto market, but also a broader shift: more users are beginning to treat stablecoins as a global financial infrastructure tool, rather than merely an investment asset.

For cross-border travel scenarios such as the 2026 World Cup, the core value of stablecoins lies in addressing three key pain points:

- Replacing Multi-Currency FX with USDT/USDC (Reducing Repeated Conversions)

For example, a fan traveling from Tokyo:

- Traditional approach: JPY → USD → CAD → MXN → JPY (at least 5 conversions)

- Stablecoin approach: JPY → USDT (one-time conversion) → direct spending across all countries

Result: No need to repeatedly exchange currencies in each country, reducing cumulative FX spread losses.

- Avoiding DCC and Dual Exchange Rate Losses

When making card payments in Canada or Mexico:

- Traditional credit cards: may trigger DCC (an additional 4%–8% cost)

- Stablecoin cards (e.g., BenPay): settle directly in USD-based logic

Result: Reduced exposure to merchant-side exchange rate markups.

- Unified USD-Based Budgeting for Easier Cost Control

For example:

- Hotel: $800

- Tickets: $1,200

- Food & transportation: $1,000

The traditional approach requires multi-currency budget tracking, while stablecoin-based systems allow a unified USD-denominated budget pool.

Result: It becomes significantly easier to control the overall World Cup travel budget.

While stablecoins themselves solve the problems of value storage and cross-border transfers, they still require a “last-mile” bridge to be usable in real-world scenarios such as hotels, dining, and retail spending. This is exactly why stablecoin payment cards have been rapidly gaining traction.

How Stablecoin Payment Cards Work in Practice

The core idea of a stablecoin payment card is to connect on-chain assets such as USDT or USDC with traditional Visa/Mastercard payment networks. Users do not need to convert stablecoins into local fiat currencies, nor do merchants need to accept crypto directly. Instead, users can simply spend as they would with a regular credit card, and the payment is settled automatically in the background.

Below, we look at several real World Cup travel scenarios to understand how stablecoin cards help travelers reduce costs and improve payment efficiency.

Scenario 1: Hotel Booking (USA → Canada Cross-Border Travel)

You fly from Los Angeles to Toronto and book a hotel priced in CAD.

Traditional method:

- Pay with credit card → 1.5% foreign transaction fee + potential 4–5% DCC markup + USD→CAD FX spread

- Total hidden cost can increase overall spending by 4–7%

Using a stablecoin payment card: You hold USDC (USD-pegged stablecoin) in your card account, so there is no need to pre-exchange into CAD. At checkout, the system automatically converts USDC into CAD at the optimal rate and completes settlement, avoiding DCC and high FX markups.

For a hotel costing 300 CAD per night, a stablecoin card can save approximately $50–$80 compared to a traditional credit card.

Scenario 2: Local Spending in Mexico (Dining + Shopping)

While attending matches in Mexico City, you pay for restaurant bills (MXN) and buy souvenirs.

Traditional method: USD cash or credit card → multiple FX conversions (USD→MXN) + ATM withdrawal fees + exposure to peso volatility.

Stablecoin method: You simply pay with a crypto-linked card. The backend automatically converts stablecoins into local currency, and the merchant receives MXN directly. You do not need to hold Mexican pesos, nor worry about leftover cash or reconversion losses after the trip.

Scenario 3: Real-Time Fund Top-Up (Urgent Ticket Purchase)

In Toronto, you are about to buy tickets for a Canada match, but prices suddenly surge and you need additional funds immediately.

Traditional bank transfer: 1–3 business days + high wire transfer fees.

Stablecoin payment card: USDC top-up completes within minutes, allowing you to pay instantly and secure the ticket during the price window.

Across all these scenarios, the common advantage is clear: you do not need to prepare different currencies for each country or repeatedly exchange money. A single stablecoin payment card is enough to cover spending across the US, Canada, and Mexico.

How BenPay Fits Into World Cup Cross-Border Travel Scenarios

For a cross-border travel scenario like the World Cup, the core challenge users face is not a lack of payment capability, but rather the accumulation of payment costs. As travelers move between the United States, Canada, and Mexico, they are repeatedly exposed to issues such as:

- Multi-currency FX conversion losses

- Foreign transaction fees on non-local currency spending

- Additional cross-border payment charges

- Fragmented fund management across multiple accounts

- Low capital efficiency due to idle pre-trip funds

Such cross-border consumption scenarios have also driven the development of stablecoin payment infrastructure. BenPay was incubated and supported by Bixin Group, and the design goal of the BenPay Card is precisely to optimize around these cross-border consumption pain points.

Unlike traditional bank cards, which rely primarily on bank accounts and fiat currency systems, BenPay is built on a stablecoin-based asset layer. It connects this on-chain value to global spending scenarios through the Visa/Mastercard network, enabling users to maintain a unified fund management system across different countries.

For users traveling frequently between countries during the World Cup, this model delivers value not only in payment convenience, but also in overall cost structure optimization. For example:

Reduced Multi-Currency Fund Preparation

In the traditional model, travelers may need to pre-convert funds such as 3,000 USD, 2,000 CAD, and 15,000 MXN. With BenPay, users only need to hold an equivalent value in USDC or USDT.

Lower Cross-Border Transaction Fees

Different BenPay card tiers are optimized for different spending behaviors and scenarios.

For example, the Sigma Card offers a 0% cross-border transaction fee structure, making it particularly suitable for users with frequent international spending needs and multi-country travel patterns.

In a World Cup scenario involving continuous movement across multiple countries, this helps significantly reduce the additional fees commonly associated with traditional bank cards.

Unified Online and Offline Spending

During World Cup travel, user spending typically spans multiple categories:

- Hotel bookings

- Flights and transportation

- Dining and retail purchases

- AI tools and online subscriptions

BenPay allows all of these expenses to be managed within a single fund system, eliminating the need to maintain multiple bank cards or separate payment accounts.

Improved Idle Fund Efficiency

For users who prepare travel budgets in advance, funds often remain unused for several weeks or even months before departure.

BenPay enables card balances to participate in on-chain yield strategies, allowing idle funds to generate potential returns instead of sitting inactive in a traditional card or bank account.

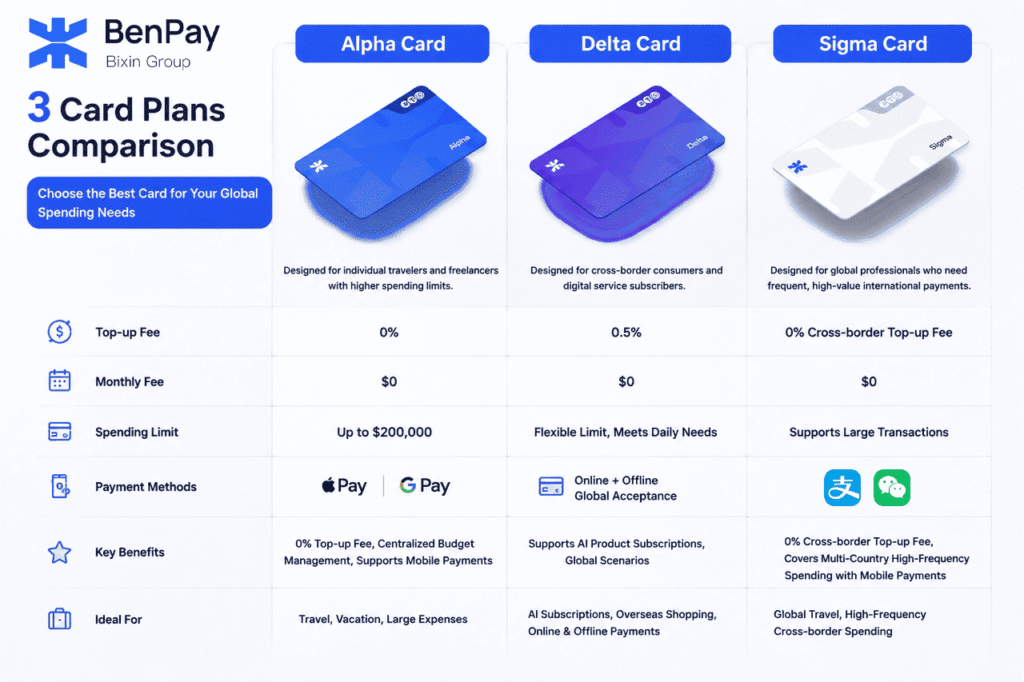

Which BenPay Card Is Best for World Cup Cross-Border Travel?

BenPay offers three card options—Alpha, Delta, and Sigma—each designed for different cross-border spending needs.

BenPay Alpha Card

Best suited for users who primarily focus on travel spending with relatively high single-transaction amounts.

Key features:

- 0% top-up fee

- No monthly fee

- Supports Apple Pay / Google Pay

- Up to $200,000 card limit

For users who want to minimize funding costs and manage a centralized travel budget, the Alpha Card is a strong baseline option for cross-border spending.

BenPay Delta Card

Designed for users who combine cross-border spending with digital subscription needs.

Key features:

- No monthly fee

- Only 0.5% top-up fee

- Supports AI subscriptions such as ChatGPT, Claude, and Codex

- Works for both online and offline global spending

For users who frequently subscribe to AI services while also traveling or spending internationally, the Delta Card offers greater flexibility.

BenPay Sigma Card

Optimized for users who need frequent cross-border mobility during the World Cup (e.g., traveling between the US, Canada, and Mexico).

Key features:

- 0% cross-border transaction fee

- Supports high-value spending

- Compatible with Alipay and WeChat Pay

- Designed for high-frequency international consumption

For long-term travelers, digital nomads, and international business users, the Sigma Card delivers the strongest cost advantage in high-frequency cross-border scenarios.

From a cost perspective, the World Cup is not just a football event—it is a magnified cross-border consumption scenario. For users moving frequently between multiple countries, reducing currency conversions, lowering cross-border fees, and unifying fund management often matters more than choosing any single bank. This is precisely why BenPay’s stablecoin payment cards are increasingly gaining attention among global consumers.

Conclusion

The 2026 World Cup is only a microcosm of a much larger trend. When millions of international travelers move across multiple countries at the same time, the limitations of today’s payment systems become dramatically amplified:

- How can cross-border payment costs be reduced?

- How can foreign exchange losses be minimized?

- How can capital flow efficiency be improved?

- How can global spending become simpler and more seamless?

These challenges will not disappear after the World Cup ends.

With the continued growth of remote work, digital nomad lifestyles, cross-border e-commerce, and globalized service trade, cross-border consumption is becoming an increasingly common way of life. From this perspective, the rise of stablecoins is not only a financial innovation, but also an upgrade of global payment infrastructure.

In the past, moving between countries meant constantly switching between bank accounts, currency systems, and payment tools. With the development of stablecoins, digital identity systems, and global payment networks, the future cross-border payment experience may increasingly resemble the internet itself—users no longer need to worry about underlying settlement paths, but simply focus on making payments.

The World Cup is just a snapshot, but it clearly reflects the transformation already underway in the era of globalized consumption. As one of the payment infrastructure products incubated under Bixin Group, BenPay is exploring how stablecoins can be integrated into real-world spending scenarios, aiming to help global users achieve more efficient cross-border payments and digital asset utilization.

For users, the ideal future of payments may not be about knowing which chain the funds come from or which network they pass through, but rather that at the moment of payment, value flows as freely as information on the internet. This may ultimately be the direction in which stablecoin payments evolve.

FAQ: 2026 World Cup & Stablecoin Payments

Q1: Why does the World Cup impact cross-border payment behavior? The World Cup drives a short-term surge in high-frequency cross-border spending, including flights, hotels, dining, and transportation. This concentrated demand amplifies existing inefficiencies in traditional payment systems, such as transaction fees, exchange rate losses, and settlement delays.

Q2: What are the advantages of stablecoin payments in cross-border travel? Stablecoins are pegged to fiat currencies such as the US dollar, which helps reduce losses from multi-currency conversions. They also enable near real-time cross-border transfers, thereby lowering overall payment costs.

Q3: What hidden costs exist when using credit cards abroad? The main costs include: international transaction fees (1%–3%), dynamic currency conversion (DCC) fees (4%–8%), FX spreads, and ATM withdrawal charges. These costs are often not obvious in a single transaction but accumulate significantly over the course of a trip.

Q4: Can stablecoins fully replace traditional payment methods? Not yet. Stablecoins primarily function as a global value transfer layer, while real-world consumption still relies on card networks or payment rails such as Visa and Mastercard to complete the “last mile” of payment.

Q5: What role does BenPay play in the payment ecosystem? BenPay connects on-chain stablecoin assets with traditional payment networks, enabling users to spend digital assets directly in real-world scenarios such as hotels, retail, and transportation.

Q6: Is using stablecoins more cost-effective during the World Cup? In scenarios involving high FX volatility and frequent currency switching (such as the US, Canada, and Mexico), stablecoins can reduce conversion frequency and related costs. However, the actual savings depend on the specific payment rails and fee structures used.

Q7: How do I use a BenPay Card? Users can sign up via the BenPay app, complete KYC verification, and top up USDT/USDC. Once funded, the card can be used anywhere that supports Visa or Mastercard payments, both online and offline.