Stablecoin Payments Go Mainstream as the Crypto Payment Card Market Rapidly Expands

Crypto spending cards are no longer just a niche product for Web3 users — they are rapidly becoming a new global payment tool.

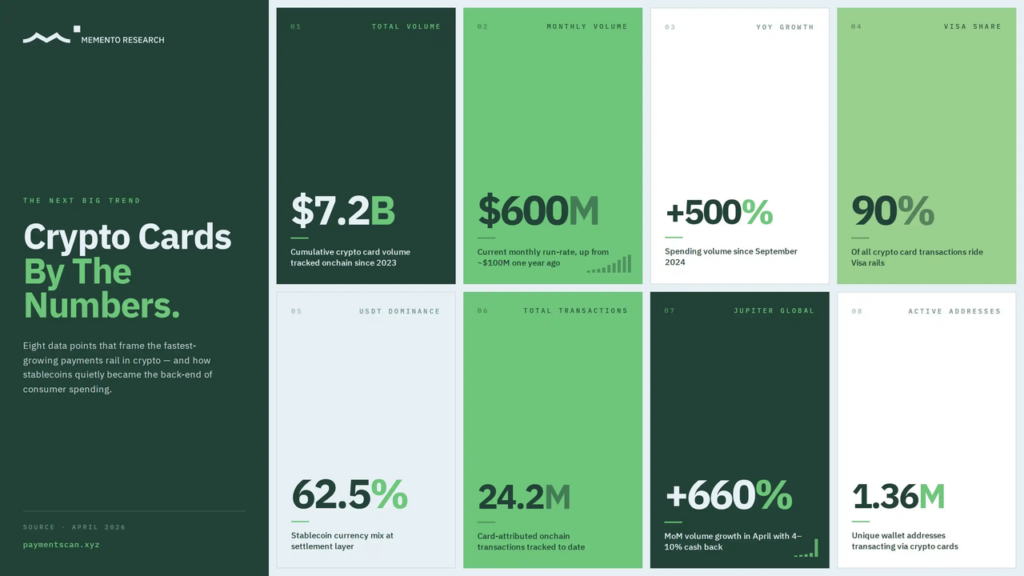

According to the latest Memento Research data, crypto card monthly spending has surpassed $600 million in 2026, representing a 6x increase from approximately $100 million one year ago.

Since 2023, the total on-chain crypto card spending volume has exceeded $7.2 billion, with over 24.2 million transactions and approximately 1.36 million unique wallet addresses involved.

More notably, 62.5% of settlement volume is dominated by USDT. This indicates that the core driving force behind crypto payment growth is no longer highly volatile crypto assets, but stablecoins that are far more suitable for everyday spending.

This is not just about transaction volume growth — it reflects crypto cards gradually evolving from Web3 niche products into real-world payment methods.

The Industry Significance of Crypto Cards Reaching $600 Million in Monthly Spending

The $600 million monthly spending milestone is no longer just a growth number — it signals a structural shift in the crypto payments industry.

In the past, cryptocurrencies were primarily viewed as investment assets or trading instruments. Today, an increasing amount of capital is flowing into real-world payment scenarios.

Unlike previous crypto cycles driven mainly by trading and speculation, this round of growth is powered more by genuine consumer demand, including:

- Growing demand for everyday spending

- Rising need for cross-border payments

- Increased adoption of stablecoins

- Continued expansion of the Web3 user base

- Gradual maturation of global payment infrastructure

This also indicates that stablecoins are gradually transitioning from “investment assets” to practical “payment tools.”

- Rapidly Growing User Acceptance of Stablecoin Payments

In the past, stablecoins were mainly active in exchanges and DeFi scenarios. Today, more and more users are directly using USDT, USDC, and others to complete real-world transactions.

Compared to highly volatile assets like BTC and ETH, stablecoins are far more suitable as a payment medium. Their relatively stable value closely aligns with users’ habits of using “digital dollars.”

Data shows this trend is already very clear. Currently, approximately 62.5% of crypto card settlement volume is dominated by USDT. This strongly demonstrates that stablecoins have become the core payment asset in today’s crypto payment system, driving the shift of crypto payments from “investment tools” to “consumption tools.”

- Crypto Consumption Scenarios Are Expanding Across the Board

Early crypto spending cards primarily served Web3-native users. Today, their usage scenarios have rapidly expanded into a much broader global consumption ecosystem, including:

- Global travel and cross-border spending

- AI tools and SaaS subscriptions

- Overseas advertising

- Digital product purchases

- E-commerce payments

- Freelancer income settlement

- In-app payments within Web3 applications

Especially against the backdrop of rapid growth in the AI economy, remote work, and digital nomad lifestyles, crypto payments are becoming the preferred payment method for more and more globalized users. Crypto spending cards are gradually evolving from “niche products” into more universal digital payment tools.

- Global Payment Infrastructure and Compliance Systems Are Gradually Maturing

In the past, immature infrastructure was the biggest obstacle preventing crypto payments from entering the mainstream. This situation has now improved significantly. Currently, approximately 90% of crypto card transactions are processed through the Visa payment network, which means:

- Users can spend money globally just like with ordinary bank cards

- Merchants do not need to understand blockchain

- Backend systems automatically handle the conversion between stablecoins and local fiat currencies

- Blockchain mainly serves as the underlying settlement layer

At the same time, the global regulatory environment — including stablecoin regulation, KYC compliance, and payment licenses — is becoming increasingly clear. The maturation of blockchain payment technology and the advancement of compliance frameworks are together laying a solid foundation for the mainstream adoption of the crypto payments industry.

- The Inevitable Trend: From Niche Pilot to Mainstream Payment

Overall, the transition of crypto spending cards from “niche experiments” to “mainstream payment” has become inevitable. Multiple factors are driving this shift: the continuous growth of digital asset users, the upgrading of global cross-border payment demand, the maturation of blockchain payment technology, and the advancement of global regulatory compliance. Together, these dimensions are propelling the Web3 payment ecosystem into a new stage.

The milestone of crypto cards reaching $600 million in monthly spending not only demonstrates the rapid expansion of the crypto payment card market size, but also signals that stablecoins are truly becoming a global payment channel.

Compared to pure asset trading, “real-world payments” are more likely to become a key direction for large-scale Web3 adoption in the next phase. This is also why more and more industries are paying close attention to trends such as the crypto payments industry, crypto payment card market size, Web3 payment ecosystem, stablecoin payment growth, and on-chain payment infrastructure development.

How Crypto Spending Card Actually Works (Simple Breakdown)

In simple terms, the core function of a crypto spending card is to seamlessly connect on-chain stablecoins with real-world consumption scenarios. The typical payment process includes the following steps:

- Users hold stablecoins (such as USDT or USDC) in their accounts;

- When a user makes a purchase, the backend payment system instantly converts the corresponding amount of stablecoins into local fiat currency;

- Merchants receive payment normally through traditional networks like Visa or Mastercard;

- The on-chain system and payment infrastructure work together to complete backend clearing and settlement.

For merchants, this process is almost identical to receiving payment from a regular bank card. For users, it enables direct spending of their stablecoin assets.

Real-World Example: You pay for a meal costing 5,000 JPY in Japan. The card automatically deducts the equivalent amount of USDT and converts it in real time. The restaurant receives Japanese Yen. You experience zero friction from cryptocurrencies, and the merchant doesn’t need to know anything about blockchain.

This model essentially achieves the perfect integration of “stablecoin liquidity + traditional payment networks.”

Next-Generation Crypto Payment Cards: The Fusion of Spending and Yield

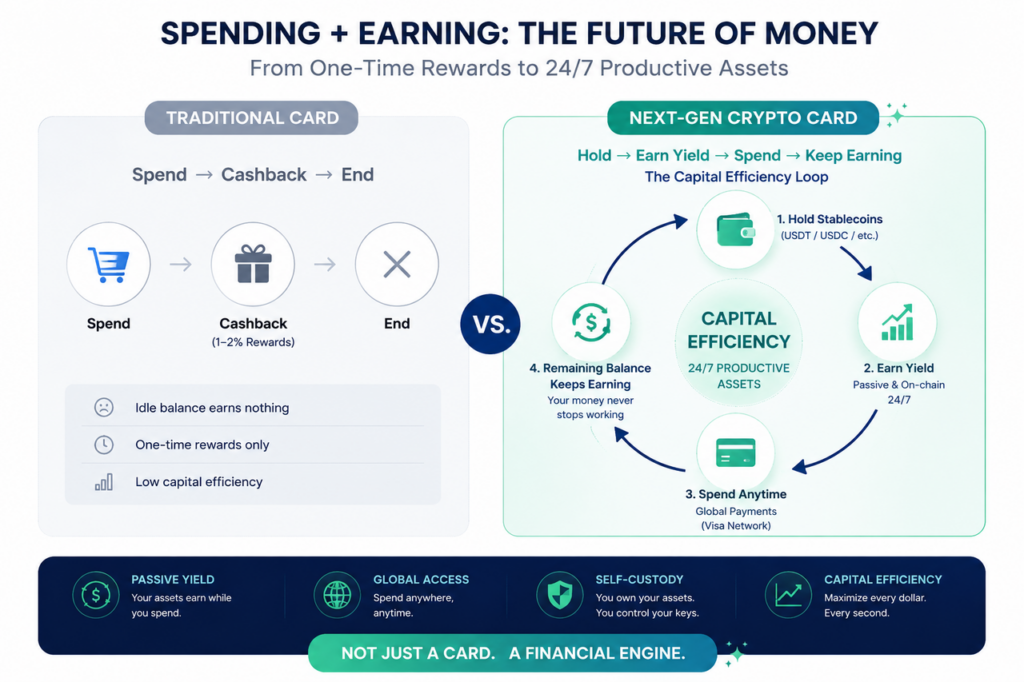

Compared to traditional bank cards, more and more crypto spending cards are now incorporating “yield-generating capabilities.”

- Traditional Credit Cards: After spending, users may earn a small cashback (1-2%) or tiered rewards depending on the card type. However, idle balances generate no returns, resulting in low capital efficiency.

- Next-Generation Crypto Cards: They allow users to continue earning yields on their funds even while spending.

For example:

- Remaining stablecoin balances continue to generate on-chain yields

- No need for long-term locking or staking

- Users maintain full spending liquidity

This creates a powerful financial loop: Top-up → Continuously earn yields → Spend anytime → Remaining balance keeps earning → Repeat

Crypto cards are evolving from simple “payment tools” into comprehensive digital financial accounts that combine both spending and yield generation. The core logic behind this is capital efficiency — users no longer have to choose between “spending” and “earning.”

To some extent, this represents a new direction born from the fusion of stablecoin payments and DeFi yields.

What to Look for When Choosing a Crypto Card in 2026?

Not all crypto cards are the same. As adoption scales, the differences between them are becoming increasingly important. Here are the core evaluation factors:

- Stablecoin liquidity (depth of USDT/USDC support)

- Yield mechanism (automatic vs manual)

- Fees and exchange rate spreads

- Global usability (Apple Pay, Google Pay, Alipay, WeChat Pay, etc.)

- Custody model (self-custody vs centralized custody)

- Yield continuity (one-time cashback vs continuous on-chain yields)

More mature crypto card products should feel as natural as using an ordinary bank card, without requiring users to understand complex on-chain logic.

User Experience Gap Remains the Biggest Bottleneck

Despite the industry’s rapid growth, most crypto card products still face the following challenges:

- Complicated onboarding processes (KYC + fragmented wallet integration)

- Manual fund management between earning yields and spending

- Lack of transparency in the yield generation process

- Interfaces that feel too “crypto-native” for average users

Therefore, the products that ultimately win in the future may not be those with the highest yields, but those that offer the smoothest and most seamless user experience.

How Solutions Like BenPay Card Address These Challenges

Next-generation crypto card products are attempting to solve the fragmentation in traditional crypto payment experiences through a fused model of “spending + yield + self-custody.”

Taking BenPay Card as an example, it integrates spending, yield generation, and self-custody into a single unified payment system. This allows users to maintain full fund liquidity while keeping their assets continuously generating returns.

Key Features Include:

- Remaining balances continuously generate on-chain yields with no need for staking or long-term locking

- Users retain full self-custody control (via wallet signature authorization)

- Supports direct top-ups from multiple chains including Solana, Tron, Ethereum, BSC, and BenFen

- Delivers a spending experience close to traditional bank cards

- Supports one-click registration and login with Apple / Google accounts, lowering the barrier to entry

- Offers multiple card types and higher spending limits

Real-World Use Cases

- Freelancers and Remote Workers: Top up their card after receiving USDT/USDC payments and enjoy continuous yields on the remaining balance while making daily expenses.

- Frequent Travelers and Overseas Shoppers: Benefit from high spending limits and seamless global payments without worrying about exchange rates or cross-border fees.

- AI Developers and Digital Professionals: Easily pay for subscriptions such as OpenAI, Claude, SaaS tools, and GPU rentals, while maintaining full liquidity and ongoing yields on their assets.

Who Is the Crypto Spending Card Suitable For?

Crypto cards are particularly suitable for the following users:

- Those who already hold stablecoins

- People who frequently make international or cross-border payments

- Users who want to earn passive yields without active management

- Those looking for alternatives to traditional banking

Future Trends

The $600 million monthly spending milestone is likely just the beginning. As DeFi yields and consumer finance become more deeply integrated, we will see more powerful and user-friendly products emerge. Key areas to watch include:

- Stablecoins gradually becoming a global payment channel

- Further integration of DeFi yields and consumer finance

- Continuous simplification of Web3 payment experiences

- Gradual maturation of global regulation and compliance systems

In the near future, the core question may no longer be “Why use a crypto card?” but rather — “Why let your money sit idle?”

The financial system of the future may no longer force users to choose between “spending” and “earning.”

Instead, it will allow capital to keep circulating and generating value while maintaining full liquidity.