Overview of the Crypto Payment Card Sector

As the penetration of crypto assets continues to grow worldwide, the number of users holding and using crypto assets is steadily increasing. For the hundreds of millions of crypto holders, beyond the need to trade for profit, there is an equally pressing demand: how to use the crypto in their wallets as seamlessly, securely, and cost-effectively as fiat currency — for online subscriptions, in-store purchases, and everyday bill payments. The crypto payment card is the most intuitive solution to this need, bridging on-chain value with real-world spending.

Crypto payment cards connect crypto assets to traditional card networks, enabling users to spend their crypto directly at any merchant that accepts Visa or Mastercard. These cards generally fall into two categories: custodial cards and non-custodial cards.

- Custodial crypto payment cards have the issuing institution (such as a centralized exchange) hold the user’s assets on their behalf. Funds are stored in the platform account, and the platform automatically converts crypto to fiat at the time of payment.

- Non-custodial crypto payment cards are linked directly to the user’s own wallet. The private key remains in the user’s control, and funds do not need to be transferred to the platform in advance — the asset deduction or fiat conversion only occurs at the moment of spending via authorization. This achieves “self-custodial” payments and reduces third-party custody risk. Currently, the mainstream crypto payment card market is still dominated by custodial models (such as cards issued by Crypto.com and Coinbase), but non-custodial solutions represented by Gnosis Pay and BenPay are emerging, reflecting a trend toward decentralization in the crypto payment card space.

The global crypto payment card market is in a phase of rapid growth, a trajectory confirmed by real on-chain payment data. According to the latest research from Artemis, crypto card transaction volume has grown from approximately $100 million per month in early 2023 to over $1.5 billion per month by the end of 2025, representing a compound annual growth rate of 106%. The annualized transaction volume now exceeds $18 billion, nearly on par with stablecoin peer-to-peer payment volume (approximately $19 billion). This shift indicates that crypto payment cards have evolved from an early niche tool into core infrastructure connecting stablecoins with real-world consumption. At a macro level, the total stablecoin transfer volume has reached tens of trillions of dollars — surpassing Visa by some measures — providing an abundant “funding source” for continued crypto card growth.

From a geographic perspective, crypto payment card penetration shows clear stratification. North America and Europe remain the most mature markets. Europe, benefiting from regulatory clarity (such as the gradual rollout of the MiCA framework) and unified payment infrastructure like SEPA, has developed a relatively mature crypto payment ecosystem. Early participants such as Wirex and Bitstamp have driven the behavioral shift among users from “holding crypto” to “spending crypto.” European users’ high acceptance of electronic payments and multi-currency accounts has also lowered the education barrier for crypto cards. The North American market, meanwhile, is more compliance-driven. With licensed platforms such as Coinbase and Gemini leading the way, crypto payment cards have gradually integrated into mainstream finance. Users in this region tend to view crypto cards more as asset management and cashback tools than as basic payment instruments.

At the same time, emerging markets are becoming the most significant source of new growth. In Latin America, Southeast Asia, and the Middle East, high local currency volatility, elevated inflation, and underdeveloped banking infrastructure have led stablecoins (especially USDT and USDC) to increasingly serve as “quasi-dollar accounts,” widely used for value storage, cross-border remittances, and freelance settlements. In high-inflation economies such as Argentina and Turkey, stablecoins have become an important tool for residents to hedge against local currency depreciation. In labor-exporting countries like the Philippines and Vietnam, on-chain dollars are gradually replacing traditional remittance channels. In this context, crypto payment cards play a critical “last-mile” role — converting on-chain dollar balances directly into offline spending power (for everyday shopping, subscription services, ad spending, and more) — completing the full loop of “store, transfer, spend.” This is why the demand for crypto cards in emerging markets is fundamentally about replacing payment infrastructure, rather than merely experimenting with financial innovation.

Overall, the growth logic of crypto payment cards is undergoing a fundamental shift: from reliance on crypto trading activity and user growth, toward real consumption driven by stablecoin payment demand. In the absence of large-scale merchant support for direct stablecoin payments, crypto cards will continue to serve as the core bridge between on-chain assets and global payment networks, and are poised for sustained high growth alongside the broader expansion of the stablecoin ecosystem.

The Crypto Payment Card Industry Chain

The crypto payment card industry chain is, in essence, the complete pathway for connecting crypto assets to the traditional card network clearing system, with each link fulfilled by different participants working in coordination.

Card Issuers

Card issuers are the entities responsible for providing crypto payment card services to users. They are typically leading centralized exchanges (CEXs) and mainstream wallet providers — such as Coinbase, Bybit, Bitget, and Crypto.com. Leveraging their large user bases, these issuers extend their platforms’ asset monetization channels into offline spending networks by offering physical or virtual cards.

Issuers generally develop user-facing applications and card management services, and coordinate compliance efforts with issuing banks. They also manage users’ fund accounts and handle the conversion between crypto and fiat at the time of payment. To attract users, issuers typically offer rewards such as cashback, points, and subscription rebates. It is worth noting that most crypto companies do not hold banking licenses themselves. Their card products therefore require partnerships with licensed financial institutions (commonly referred to as BIN sponsors) to indirectly obtain the authority to issue Visa or Mastercard card numbers.

BIN Sponsors

BIN stands for Bank Identification Number — the first 6 to 8 digits of a bank card number that identify the issuing financial institution. For example, a Visa card number typically consists of 16 digits starting with “4,” with the first 6 digits representing the issuing bank’s BIN. BIN sponsors are banks or electronic money institutions that hold a BIN and possess card issuance qualifications. Since most crypto companies lack these credentials, they partner with licensed issuers who provide the BIN and bank card accounts, formally connecting the card to the Visa or Mastercard network.

The typical arrangement between card issuers and BIN sponsors is a white-label card program: the crypto platform handles the user interface, card branding, currency conversion, and customer service, while the BIN sponsor is responsible for card generation and clearing, fiat custody, and connecting to the Visa/Mastercard network. For example, Coinbase partnered with BIN sponsors such as Paysafe and Wirecard to issue the Coinbase Card.

Card Networks

Card networks — also known as payment card organizations or card schemes — are international payment networks responsible for setting transaction standards for bank card payments, maintaining merchant networks, and providing clearing capabilities. Major examples include Visa, Mastercard, UnionPay, and American Express. Card networks do not issue cards themselves; cards are issued by their member financial institutions (primarily banks). The networks themselves serve as “payment infrastructure,” handling the exchange of transaction information, rule-setting, transaction standards, and fund clearing. Both Visa and Mastercard are highly active in the crypto card space, and the vast majority of crypto cards are issued in partnership with one of them. Visa’s partners include Coinbase, Crypto.com, Bitget, and Wirex, while Mastercard’s include Bybit, Wirex, Gemini, and Nexo.

Technology Service Providers

In addition to the main participants above, various technology providers play supporting roles — most notably payment processors and KYC service providers.

Payment processors handle the technical workflow of card transactions on behalf of issuers and BIN sponsors, including transaction authorization (real-time approval decisions), card lifecycle management (card issuance, suspension, and cancellation), and transaction routing. For instance, Coinbase Card uses the Marqeta platform: every time a user makes a purchase, Marqeta’s Gateway system calls Coinbase’s account balance API in real time to authorize the transaction.

KYC service providers supply card issuers with identity verification and risk assessment services, encompassing Know Your Customer (KYC) checks and Anti-Money Laundering (AML) screening. Crypto card issuers typically integrate third-party identity verification services (such as SumSub and Onfido) to verify user identities, ensure the legality of cardholders and the compliance of fund sources, and meet regulatory requirements for prepaid and debit card issuance — laying a lawful foundation for the payment process.

Merchants and POS Terminals

Merchants, along with their POS terminals or payment gateways, are an indispensable link in the crypto payment card ecosystem. When a cardholder initiates a payment, the transaction request enters the traditional card network through the terminal for processing.

In most cases, the merchant experience with a crypto payment card is no different from that of a regular bank card: the transaction is settled in local fiat currency, funds are cleared through the acquiring bank via standard processes, and merchants generally have no need to know whether the funds originated from crypto assets.

In certain specific scenarios — such as merchants with a cooperative relationship with the card issuer, or high-risk industries that are more sensitive to the origin of funds — merchants or acquiring banks may have heightened awareness of or stricter risk controls around transaction types and fund sources.

Overall, by leveraging global card networks like Visa and Mastercard, crypto payment cards seamlessly integrate into the existing payments ecosystem, extending the usability of on-chain assets to every merchant that accepts traditional bank card payments.

Payment Flow and Risk Control

Payment Flow

When a cardholder makes a purchase at a merchant using a crypto card, the process unfolds as follows:

- Transaction Authorization: After the cardholder initiates a payment, the POS terminal sends the transaction request (containing merchant information, transaction amount, currency, etc.) through the acquiring bank to the card network, which routes it to the card issuer’s system. Upon receiving the request, the issuer (or its payment processor) first verifies the card’s validity and account status, then checks whether the user’s crypto or fiat balance is sufficient to cover the transaction.

- For cards using Just-In-Time (JIT) Funding, the issuer triggers a real-time crypto-to-fiat conversion at this moment: the equivalent amount of the user’s crypto assets is sold or deducted at the current market price, providing sufficient fiat funds to authorize the transaction. For example, Coinbase Card uses Marqeta to instantly sell the user’s chosen cryptocurrency via API upon receiving each transaction request, converting it to USD before authorizing the transaction. The advantage of JIT is that users do not need to pre-convert assets to fiat, making capital utilization more efficient; the issuer also avoids holding large fiat balances on behalf of users (reducing compliance pressure and interest costs). The technical challenge lies in the need for low-latency, high-reliability trade execution interfaces, as well as risk models that ensure every transaction is fully covered before approval.

- For prepaid cards — such as those issued by Crypto.com. Users pre-convert their crypto to fiat and load it into the card account. Authorization simply checks whether the card’s fiat balance is sufficient, with no real-time conversion needed.

- The authorization stage is critical, as it determines whether a transaction is approved or declined. Once approved, the corresponding funds are locked upstream, and the card network returns an authorization code to the merchant as confirmation of payment.

- Fund Loading / Deduction: After authorization, the platform deducts the corresponding assets from the user’s account. The method varies depending on the card architecture.

- Custodial cards typically deduct the crypto balance in the backend and record the change in the internal ledger.

- Non-custodial cards may transfer the corresponding token amount from the user’s on-chain wallet to the issuer’s address or a custodial smart contract via a smart contract. Since a traditional POS transaction completes in a matter of milliseconds — far too fast to wait for a blockchain transaction confirmation — these solutions typically achieve instant deduction through pre-authorization or off-chain trust mechanisms. For example, Gnosis Pay creates a payment network on the Gnosis Chain, where the user’s self-custodial wallet is bound to a Visa-certified contract; when the user swipes, the contract automatically executes the deduction, transferring stablecoins from the user’s on-chain account to a designated clearing account. Another approach requires users to pre-deposit funds into a specified on-chain address or Layer 2 network. For instance, MetaMask Card requires users to deposit USDC/USDT and other assets into a designated contract account on Ethereum’s Linea network; at the time of purchase, the corresponding tokens are deducted directly from that contract. On-chain deduction solutions are mostly still in early stages, but they represent an important step toward a fully trustless crypto card.

- Regardless of the approach, the goal of fund loading is to ensure the issuer holds the necessary fiat funds to pay the merchant.

- Clearing: Clearing refers to the process of formally recording transactions and settling funds between financial institutions. Typically at the end of the business day, card networks like Visa and Mastercard calculate the net receivables and payables between the merchant’s acquiring bank and the card issuer, then initiate clearing instructions. In traditional cross-border or cross-currency scenarios, the issuer must convert currencies and remit funds to the acquiring bank via SWIFT or similar networks — a process that can take several days. However, Visa has explored using blockchain-based stablecoins for direct settlement: for example, Visa allows issuers to transfer settlement funds in real time via USDC on-chain, replacing the time-consuming bank wire transfer.

- Once clearing is complete, the merchant receives payment in local currency in their bank account, and the issuer’s account is debited accordingly. In terms of crypto price volatility risk: under the JIT model, since fiat is locked at the moment of authorization, the issuer bears virtually no exchange rate risk. Under the prepaid model, the user absorbs price volatility at the time of top-up, so there is no currency value risk at the point of spending.

3.2 Risk Control

Since crypto payment cards involve both fiat payments and crypto assets, risk control must address both traditional payment risks and crypto-specific risks:

- Transaction Fraud Monitoring: Like ordinary credit or debit cards, crypto cards face risks such as unauthorized use and counterfeit card transactions. Many platforms allow users to freeze or unfreeze their card directly in the app; if a suspicious transaction is detected, the user can immediately lock the card to stop further payments. Since most crypto cards are debit cards with no credit line, losses from unauthorized use primarily affect the user’s own assets. This places greater responsibility on issuers to protect user account security through measures such as two-factor authentication (2FA) and alerts for suspicious login activity.

- Crypto Asset Price Volatility Risk: Extreme fluctuations in cryptocurrency prices can impact the payment process. If a user’s assets are sufficient at the time of authorization but their value drops sharply by the time of clearing, the issuer may receive insufficient crypto assets to cover fiat expenditures. To mitigate this, most JIT-model platforms complete the conversion and lock in the fiat amount at the moment of authorization, effectively passing the price risk to the user (who is, in effect, selling their crypto at market price at the time of purchase). Under the prepaid model, the user absorbs price volatility at the time of top-up; since the account holds stablecoins or fiat after reloading, there is no currency value risk at the point of spending.

- System Security and Operational Continuity: Crypto card systems must guard against both blockchain-level security threats (such as hacking and private key management) and traditional IT risks (such as database breaches and DDoS attacks). Most platforms store users’ crypto assets in multi-signature cold wallets or with trusted custodians to minimize the risk of theft. Card systems require disaster recovery plans with redundant servers deployed across multiple global locations, and coordination with card networks to enable rapid channel failover. In the event of a partner bank or payment processor outage, the issuer must urgently seek alternatives to maintain card availability for users.

Business Model of Crypto Payment Cards

The business model of crypto payment cards is built on the traditional bank card framework, combined with fee structures and reward mechanisms unique to the crypto industry.

Revenue Sources

- Conversion Spread Revenue: When users convert digital assets to fiat currency through a crypto card, the issuer typically captures a spread in the exchange rate, generating implicit income. For example, if a user converts BTC to receive $100 in fiat, the platform may deduct BTC worth $101 — the extra $1 effectively represents the platform’s conversion fee. Many cards claim “zero-fee conversion,” but in practice the fee is embedded in the exchange rate spread. Spreads vary by platform and asset type; stablecoin-to-fiat conversions tend to carry smaller spreads due to lower volatility. Spread revenue benefits from economies of scale: the higher the transaction volume, the more significant the cumulative income.

- Transaction Fees: Each card purchase generates a Merchant Discount Rate (MDR) paid by the merchant, a portion of which — the interchange fee — accrues to the card issuer. In addition, some crypto cards charge users a direct transaction fee (typically 0.5%–2%) or a top-up fee (typically 1%–2%).

- Service and Management Fees: Some crypto cards charge card management fees or fees for specific services, such as physical card issuance and shipping fees, monthly account maintenance fees, currency conversion fees, foreign transaction fees, and ATM withdrawal fees. Many leading products have eliminated annual fees and card issuance fees and offer a certain amount of free ATM withdrawals. Premium cards may charge annual fees but provide higher-tier benefits such as airport lounge access and insurance coverage.

- Interest Income: Users’ pre-deposited fiat or stablecoin balances sitting in platform accounts can be deployed by the platform to generate returns — for example, by placing funds in money markets or providing liquidity. This is similar to the interest spread on demand deposits in banking, though it requires careful balance of risk and compliance.

- Token Economy Revenue: Many issuers have their own platform tokens (such as Crypto.com’s CRO and Bitget’s BGB). They leverage the crypto card business to expand the utility of these tokens — for instance, by requiring users to hold a certain amount of the platform’s token to access higher-tier cards or higher cashback rates, and by issuing cashback rewards in the form of the platform’s own token, thereby creating demand and liquidity for it. For example, Crypto.com’s highest-tier Obsidian card requires staking CRO tokens worth $500,000 to unlock 5% cashback.

Subsidy Strategy

Many crypto card issuers initially offer generous cashback and various subsidies to attract users — sometimes as high as 1%–5% or more. Since high cashback rates often exceed fee revenue, the shortfall must be covered by the issuer’s own funds or token reserves. To manage this, issuers typically implement a tiered cashback structure: the base tier (requiring no token staking) might offer only 1%–2% cashback, while higher tiers require users to lock up a certain amount of platform tokens to access better rates — effectively locking in user assets and reducing liquidity. Take the Crypto.com Visa Card as an example: as users increase their staked CRO holdings, their cashback rate in CRO tokens gradually rises from 0% to a maximum of 5%.

Major Crypto Payment Card Products

Before comparing specific crypto payment card products, it is necessary to establish a unified analytical framework. Given that different products vary significantly in architecture, fee design, and target audience, comparisons along a single dimension can easily produce misleading conclusions. This article therefore takes a multi-dimensional approach to systematically break down and compare the leading crypto payment cards on the market.

Evaluation Dimensions

The crypto payment card space has become increasingly diverse, with participants ranging from top centralized exchanges (CEXs) and mainstream wallet providers to independent fintech startups — all launching products with vastly different forms. Cards differ enormously in application requirements, supported regions, fee transparency, fund security models, and distinctive features. To enable systematic comparison, we focus on the following key dimensions:

- Accessibility & Onboarding: This covers the target user geography, KYC requirements and complexity, the smoothness of the registration and application process, and how the card links to existing accounts (exchange or wallet). This determines whether users can obtain and start using a crypto card, and how easily they can do so.

- Underlying Model & Trust: This examines the fund custody and transaction processing logic behind the card. Does it rely entirely on the credit backing of a centralized institution (such as an exchange or issuing platform) to hold funds, or does it partially or fully incorporate on-chain elements (such as smart contracts or user wallet signatures) to enable a non-custodial model — enhancing transparency and user control? This directly relates to the foundation of fund security and user trust.

- Cost Structure: This includes card issuance fees, annual/monthly fees, top-up/deposit fees, domestic/international transaction fees, currency conversion fees (often a hidden cost), and ATM withdrawal fees.

- Features & Functionality: This covers the supported card networks (Visa, Mastercard, etc.), the range of crypto assets available for top-up and spending, spending and withdrawal limits, whether cashback or rewards are offered, whether on-chain yield generation is available, whether localized payment methods are supported (such as Alipay or WeChat Pay binding), and any unique DeFi integrations or additional services (such as IBAN accounts).

- User Experience & Support: This encompasses softer factors such as the usability of the associated app or web interface, transaction processing speed as perceived by the user, and the availability and responsiveness of customer service channels.

CEX-Backed Crypto Payment Cards

This category of crypto payment cards is typically deeply integrated with exchange accounts, allowing users to spend directly from their trading balances. Most major exchanges have launched their own crypto payment cards, including Coinbase, Bitget, Bybit, and Crypto.com. Across the key evaluation dimensions:

- Accessibility: Bybit Card attracts users with its relatively low barrier to entry and its comparatively friendly approach to certain Asian regions (including reportedly accepting KYC from mainland Chinese users). Coinbase Card has strict geographic restrictions, currently limited primarily to users in the United States (excluding Hawaii), the United Kingdom, and Europe. KYC is a universal requirement across this category.

- Trust Model: These cards are broadly custodial in nature — user funds must be held in the exchange account, with the platform handling asset conversion and settlement at the time of payment. Under this model, the security of user funds depends to varying degrees on the exchange’s security infrastructure, risk management capabilities, and regulatory compliance. There are significant differences in transparency and risk control across exchanges: leading compliant platforms such as Coinbase typically feature more robust disclosure mechanisms (such as public company audits and proof-of-reserves) and are subject to stronger regulatory oversight; while some regional or offshore exchanges (such as Bybit and Bitget) offer greater flexibility and accessibility, but may differ in transparency, regulatory coverage, and user protection mechanisms. Although all fall under the custodial model, there is clear stratification across platforms in terms of security, transparency, and the basis for user trust.

- Cost: Bybit currently claims no annual fee and offers relatively competitive rates. The Coinbase Card charges no transaction fees at point of sale, but buying, selling, or trading crypto incurs a spread; ATM withdrawals may be subject to fees charged by the terminal operator (see the cardholder agreement for details). The Bitget Card (Asia-Pacific credit card) waives annual fees and issuance fees for virtual cards; the primary costs are a 0.9% asset conversion fee and a 1% foreign currency transaction fee (FX fee) for non-USD spending. FX fees are a cost that exists across the board in this category.

- Features: These cards support a wide range of assets held within the exchange account, and spending limits are generally high. The Coinbase Card offers cashback for US users. However, this category lacks direct integration with DeFi protocols or on-chain operations. Crypto.com’s higher-tier cardholders can enjoy perks such as Spotify and Netflix subscription rebates and airport lounge access.

- Experience: For existing exchange users, card activation and day-to-day use are relatively straightforward.

Representative products in this category include:

Coinbase Card

The Coinbase Card is a Visa prepaid debit card issued by Coinbase, primarily targeting users in the United States (excluding Hawaii), the United Kingdom, and Europe, and accepted at all Visa-supported merchants worldwide. In terms of fee structure, the Coinbase Card has no annual fee, and transactions are converted at real-time exchange rates. Coinbase does not charge a fee for ATM cash withdrawals, though users may be subject to fees charged by third-party ATM operators. The card supports cashback rewards on both fiat and crypto spending; the cashback rate is dynamically adjusted, typically ranging from approximately 0.5% to 1% (and potentially higher during promotional periods). Users can choose from reward currencies including BTC, ETH, USDC, and XLM.

That said, the Coinbase Card has some notable limitations. It has not yet expanded to Asian or other international markets, which restricts the experience for global users. Customer service response times are slow, with some users reporting difficulty obtaining timely support in urgent situations such as account freezes. The cashback rate and eligible reward currencies are subject to periodic changes, making long-term planning less predictable.

Coinbase has also recently launched the Coinbase One Card credit card (running on the Amex network), specifically targeting its subscription members and offering Bitcoin rewards based on portfolio holdings — further segmenting its payments product line. Overall, this card suite is best suited for users already deeply embedded in the Coinbase ecosystem in the US or Europe.

Crypto.com Visa Card

The Crypto.com Visa Card is a crypto payment card issued by the Crypto.com exchange. It currently operates on a dual-track “Level Up” system combining subscription tiers and staking requirements. Users can choose their card tier based on their needs. With the exception of the entry-level Midnight Blue (which is free), all other tiers require users to either pay a monthly subscription fee (approximately $4.99/month for Ruby, $29.99/month for Jade) or stake CRO tokens for 12 months (ranging from $500 to $500,000 depending on the tier). Free ATM withdrawal limits are set by card tier (ranging from $200 to $1,000 per month), with a 2% fee on amounts exceeding the limit. When activated, cashback rates range from 2% to 5% (0% if not activated), and mid-to-lower tier cards have monthly cashback caps ($25–$75). Higher-tier cards provide airport lounge access and permanent Spotify/Netflix rebates; for mid-to-lower tier users, subscription rebate benefits are currently generally limited to the first 6 months.

The card’s benefits require a relatively high threshold to unlock, and the reward rules and cashback rates have changed frequently over time. Users also bear the risk of CRO token price fluctuations during the 12-month staking lock-up period. Customer service response speed and account risk control have been recurring pain points cited in user feedback.

CoinJar Card

The CoinJar Card is a crypto payment card launched by CoinJar, an established Australian exchange, running on the Mastercard network. Users do not need to stake platform tokens, and there are no annual or monthly fees. Users simply need to hold crypto assets in their CoinJar account; at the time of purchase, the system automatically sells the equivalent amount at market price to complete the fiat payment.

The card’s strengths lie in its simplicity and low barrier to entry. All spending incurs a 1% fee, but this is returned in the form of Rewards points (1 point per $1 spent), making the overall experience effectively fee-free. Apple Pay and Google Pay are both supported, covering everyday payment scenarios online, in-store, and at ATMs. One important note: cross-border transactions in currencies other than Australian dollars (AUD) incur a 2.99% foreign exchange conversion fee.

In terms of user experience, the card is fully managed within the CoinJar App, with clear and intuitive flows for card activation, switching spending assets, freezing the card, and viewing transaction history. Transaction processing speed is perceived by users as comparable to a standard bank card — swipes and mobile payments typically complete in seconds. Customer support is primarily available through an online help center and ticketing system, which handles standardized queries well but may experience slower response times during peak periods.

The card’s main limitations are its tight binding to the CoinJar custodial exchange account (no support for self-custodial wallet spending), and the absence of premium perks such as high cashback rates, subscription rebates, or airport lounge access. It is best suited for Australian users who want to use crypto assets for everyday payments and prioritize reliability.

Bitget Card

The Bitget Card ecosystem is built primarily on top of the Bitget exchange account, representing a typical centralized custodial crypto payment solution. Users can spend directly using crypto assets held in their account (such as USDT and USDC), with the system automatically converting crypto to fiat in real time at the point of transaction, enabling payments at any Visa or Mastercard merchant worldwide.

In terms of product structure, Bitget does not offer a single card but rather a suite of products targeting different regions and user groups (including a standard credit card and a premium payment card). The core proposition across the range is seamless account integration, instant conversion, and a tiered spending limit system: users can complete payments without manually pre-converting to fiat, and card tiers are tied to trading activity or VIP level, with higher-tier users unlocking greater spending limits (up to several million dollars) and cashback rewards (such as BGB cashback).

On fees, Bitget Card follows a “low visible barrier, pay-at-transaction” model: most cards have no annual fee, but transactions typically incur approximately 0.9% in fees plus around 1% in foreign exchange conversion costs; ATM withdrawals carry both fixed and percentage-based fees. Overall, the fee structure sits at a mid-market level, with the primary revenue source remaining the spread on crypto conversion and payment processing.

In terms of user experience, Bitget Card is deeply integrated with the exchange account, allowing users to open a card, manage assets, and configure spending settings directly within the app. Virtual cards can be activated quickly and linked to mainstream payment tools such as Apple Pay and Google Pay (with local payment tools supported in certain regions). However, funds remain under the platform’s custodial model, leaving users reliant on the exchange’s security infrastructure and risk management systems. Overall, these products are best suited for users already active within the Bitget ecosystem, particularly those with high trading frequency or large spending needs.

Bybit Card

Bybit is one of the world’s leading crypto exchanges by derivatives trading volume, founded in Dubai in 2018. Its registered user base reached 80 million by the end of 2025 (up from 50 million at the start of the year). It is worth noting that in February 2025, Bybit suffered a major cyberattack in which approximately $1.4 billion in ETH was stolen; the platform restored its reserves within 72 hours and honored all user assets in full. On the regulatory front, Bybit has obtained a Virtual Asset Platform Operator license from the UAE’s Securities and Commodities Authority (SCA), and its MiCAR license in Austria provides compliance coverage across the European Economic Area.

The Bybit Card, issued in partnership with Mastercard, is a crypto debit card available in both virtual and physical form. Physical cards typically carry an issuance fee (starting from approximately 5 USDT, varying by region). The card supports direct spending in multiple cryptocurrencies including BTC, ETH, USDT, USDC, XRP, and TON. Funds are deducted from the fiat balance first; if insufficient, crypto assets are automatically converted to fiat at Bybit’s quick-sell rate plus a 0.9% conversion fee. FX fees are typically in the 1%–2% range depending on region and card type. The first $100 USD in monthly ATM withdrawals is free of platform fees; amounts above this incur approximately a 2% fee, though third-party ATM operator fees may still apply. There is no annual fee. Cashback is available based on VIP tier and promotional activity, and subscriptions to services such as TradingView, ChatGPT, Netflix, Spotify, and Amazon Prime are eligible for 100% rebates. Virtual cards support Apple Pay and Google Pay for online and in-store use; physical cards additionally support contactless POS payments and ATM withdrawals.

Bybit Card is currently available to users in the European Economic Area, Switzerland, Australia, Brazil, Argentina, Mexico, and the Asia-Pacific region. Users in restricted regions (such as mainland China) should independently assess compliance and risk before applying. Virtual cards are typically issued within minutes of completing standard identity verification, though some reviews may take up to 7 business days. Overall, Bybit Card’s greatest strengths are its zero annual fee, strong cashback program, and seamless integration with the exchange account — allowing users to manage trading, savings, and spending in one place, with 24/7 multilingual customer support. Its drawbacks include a relatively limited range of supported crypto assets (primarily major coins and stablecoins), and user reports in some regions of opaque card risk controls and delayed reward payouts. Users are advised to carefully review local fee schedules and terms before applying.

Self-Custodial Wallet / DeFi-Based Crypto Payment Cards

This category of crypto payment cards is more closely aligned with the habits of Web3 users, attempting to combine payment cards with self-custodial wallets or DeFi protocols. Representative products include SafePal Card (x Fiat24), MetaMask Card, and 1inch Card. Across the key evaluation dimensions:

- Accessibility: SafePal operates by opening a compliant euro virtual IBAN account on the Arbitrum chain, and is currently available primarily to users in Europe and parts of Asia (KYC via Fiat24 is required). MetaMask Card has launched first in the European Economic Area (EEA) and the United Kingdom; users apply directly within the MetaMask wallet, with infrastructure provided by Baanx. The 1inch Card follows a unique model that requires users to collateralize assets.

- Trust Model: A hybrid model. Assets may still be held in custody by a partner, but transaction authorization is more tightly linked to the user’s wallet. MetaMask and 1inch place greater emphasis on the connection to the user’s own wallet. Transparency is generally better than pure exchange cards, but implementation varies significantly across products.

- Cost: MetaMask Card fees are relatively low. SafePal’s costs must account for Fiat24’s fee structure. The 1inch Card involves borrowing interest rather than direct spending fees.

- Features: SafePal’s real IBAN account functionality is a standout feature. MetaMask supports mainstream stablecoins such as USDC. The 1inch Card’s “borrow-to-spend” model is unique and well-suited to a specific segment of DeFi users.

- Experience: These products better match the operational logic of experienced Web3 users and support “on-chain assets, offline spending.” However, the involvement of gas fees, authorization operations, and more complex KYC processes still presents a barrier for ordinary newcomers.

Representative products in this category include:

SafePal Card

SafePal Card is built on the SafePal wallet application and is primarily available to users in Europe and select other regions. Users do not need an existing exchange account — a SafePal wallet is all that is required to apply. Upon passing Fiat24’s verification, a virtual Visa card is instantly generated and seamlessly linked to the SafePal App.

SafePal Card’s core positioning is low fees. There are no issuance fees to open a card, and account setup and management fees are completely waived. Depositing funds by converting crypto assets to USDC and topping up the account typically incurs a 0.6%–1% deposit fee, though SafePal currently runs a limited-time promotion that refunds this fee in full — effectively making top-ups free of charge. EUR-denominated spending incurs no additional fees; non-Eurozone transactions carry a 1% currency conversion fee.

In terms of supported assets, the SafePal Card defaults to USDC as the payment asset through the Fiat24 account. Users can also convert BTC, ETH, and other cryptocurrencies to USDC in one tap within the SafePal wallet before spending. Notably, the Fiat24 account includes IBAN functionality, supporting SEPA transfers to and from other bank accounts for fiat deposits and withdrawals.

Customer support is available through two channels: SafePal’s official support (online tickets and community support) and Fiat24’s banking customer service (handling compliance and account-related issues). Based on user feedback, SafePal Card’s KYC review and card activation are relatively quick, with no burdensome proof-of-address requirements — a notably lighter experience than opening a traditional bank account. One downside is that, in response to the latest compliance requirements (such as CRS and DAC8), Fiat24 has begun requesting that users provide tax residency information to comply with international tax transparency standards.

MetaMask Card

MetaMask Card is a crypto debit card service launched by the well-known decentralized wallet MetaMask. Piloted on a limited basis from 2024, it is currently available in the United Kingdom, the European Union, Switzerland, the United States, Brazil, Mexico, Colombia, Argentina, and Canada. Users must have a MetaMask wallet; there are no age or asset requirements.

The defining feature of MetaMask Card is its non-custodial model: funds remain under the user’s control in their personal wallet, with spending authorization granted to the card’s smart contract only at the time of purchase, up to a pre-approved limit. Users bridge the funds they wish to spend (supporting USDC, USDT, wETH, and others) to ConsenSys’s own Linea Layer 2 network and pre-approve the card contract to use a specified token allowance. When the user makes a purchase, the card provider deducts the equivalent amount of tokens from the user’s Linea wallet in real time via the smart contract and settles the transaction in fiat.

MetaMask Card offers two tiers: a free tier (no annual fee) and a Metal tier (annual fee of $199). Virtual card issuance and management are free on the free tier, though replacing a physical card carries a fee (replacement fee for Metal tier is $99). On transaction fees: spending with locally denominated stablecoins (USDC/USDT) is typically fee-free, with only an extremely low Linea gas fee (approximately $0.01). Using assets such as WETH incurs a 0.875% conversion fee. Spending with DeFi yield-bearing assets such as aUSDC is free up to $1,200 per month, with a 0.5% fee on amounts above that threshold. For cross-border and FX transactions: the free tier incurs a 1% cross-border fee for purchases made outside the cardholder’s home country, and non-locally denominated transactions may carry a 0.5% fee; the Metal tier waives the 1% cross-border fee. On rewards: USDC spending earns 1% cashback (paid in USDC), and Metal tier users earn up to 3% on the first $10,000 spent annually; the cashback rate reverts to 1% beyond that threshold.

Customer support is available through ConsenSys’s ticketing system and the Crypto Life/Baanx support email, currently in English only. MetaMask Card is highly accessible for on-chain users, but requires some learning investment for those with limited on-chain experience.

HyperCard (HyperPay)

HyperPay was founded in 2017 and launched its digital wallet the following year. Its core payment product, HyperCard, is designed to bridge the gap between digital currencies and everyday spending. Unlike the products described above, HyperCard began as primarily a virtual card product but has since shifted its focus to issuing and operating physical prepaid cards.

HyperCard supports over 20 major cryptocurrencies including USDT, BTC, and ETH. Its primary selling point is a streamlined application process with no traditional “country restrictions” — it is available to any user worldwide who holds a valid passport. KYC verification is provided free of charge. That said, the overall cost of card ownership is among the highest in the industry, making it more suitable for high-volume or long-term users. The total initial cost typically comprises a card issuance fee (approximately 260–269 USDT) and international shipping (approximately 100 USDT), bringing the upfront cost to nearly $400. The core ongoing costs lie in top-ups and conversions: the top-up fee is typically 3%, and each transaction may carry a 0.75% transaction fee. There is no annual fee, but given the high deposit costs, the true cost of use must be evaluated based on spending frequency. A passport is mandatory for the application. Due to the cross-border shipping and card production scheduling involved, actual delivery typically takes 2–4 weeks depending on the region, rather than the simpler 1–2 week estimate.

In summary, HyperCard is a “high-upfront-cost” crypto payment card covering over 170 countries and tens of millions of merchants. Its strengths lie in broad compatibility and the absence of any staking requirements. Its weaknesses are the high barrier to entry (in terms of fees) and expensive top-up costs. Overall, it is better suited as a backup tool for large cross-border payments rather than a primary card for small, frequent everyday purchases.

Fintech Company-Issued Crypto Payment Cards

This category is primarily issued by centralized technology companies, with representative products including RedotPay Card and Nexo Card. Across the key evaluation dimensions:

- Accessibility: RedotPay explicitly serves users in Hong Kong, Macau, Taiwan, and parts of Southeast Asia, with a relatively straightforward application process. Nexo Card is primarily available to residents of the European Economic Area (EEA).

- Trust Model: Most are led by centralized fintech companies, requiring users to trust the issuing platform.

- Cost: RedotPay’s fees are mid-range and reasonably competitive. Nexo Card’s core selling point is cashback of up to 2% (in NEXO tokens or fiat), though this is subject to loyalty tier requirements — it functions more like a crypto credit card in practice.

- Features: RedotPay’s support for binding local payment methods such as Alipay and WeChat Pay is a regional advantage. Nexo Card’s credit-and-cashback model is highly appealing.

- Experience: Regional cards may offer superior localization for their target markets.

Representative products in this category include:

RedotPay Card

RedotPay Card targets a global audience, supporting multiple languages and a wide range of regions (its official website is available in over ten languages including English, Simplified Chinese, Arabic, Spanish, and Hindi). Despite RedotPay’s commitment to global service, strict geographic restrictions apply due to compliance and card network requirements. Users from mainland China, the United States, Singapore (international version), and sanctioned or high-risk regions such as Russia, Iran, and Ukraine are currently unable to apply for virtual or physical cards. Applicants must provide identity documentation and a billing address from a non-restricted region to complete KYC.

RedotPay does not require applicants to have an existing exchange or wallet account; new users can purchase crypto directly through the app and top up their card. RedotPay Card operates under a centralized custodial model — users must deposit crypto assets into the RedotPay wallet account, where they are held by a regulated custodial trust institution. Multiple blockchain networks are supported for deposits, including BTC and ETH mainnets as well as Solana, BSC, and Tron, making it easy for users to transfer assets in.

On fees: virtual cards carry a one-time application fee of $10; physical cards cost $100. Account maintenance is completely free, with no monthly or annual fees. Transactions in non-default currencies incur a 1% crypto conversion fee plus a 1.2% foreign currency transaction fee. Minor fees also apply in certain cases, such as a $0.20 fee per small authorization transaction (≤$1) after the first five such transactions per month (which are free). RedotPay uses real-time market exchange rates with no embedded spread.

RedotPay offers a polished mobile app for card and fund management, where users can view balances (in both fiat and equivalent crypto), transaction history, and fee breakdowns in real time. Customer support is available 24/7 via in-app chat or email, in English and select local languages. User feedback indicates that responses to standard account issues are timely, though compliance-related queries may take several days to resolve. Note that ChatGPT4, Spotify, OpenAI, and Wise are currently not supported.

Nexo Card

Nexo Card is a crypto payment card issued by the crypto financial services platform Nexo. Its defining feature is the ability to seamlessly switch between “Debit Mode” and “Credit Mode” with a single tap. In Debit Mode, users spend directly from their stablecoin or crypto asset balance. In Credit Mode, users can access a credit line by collateralizing their assets — without selling them — enabling payment while retaining their holdings and unlocking liquidity. The card runs on the Mastercard network, supports Apple Pay and Google Pay, and can be used for both online and in-store purchases at merchants worldwide.

Nexo Card has strict geographic restrictions and is currently available only to users in the EEA, the United Kingdom, and certain other European countries. Users must hold a KYC-verified Nexo account to apply for a physical or virtual card.

On fees and rewards: Nexo Card charges no annual, monthly, or inactivity fees. Virtual cards can be activated once the account balance reaches a threshold of approximately $50; physical cards typically require a higher asset threshold (e.g., $5,000 or above at the corresponding tier). The card is not entirely “zero FX fee” — it charges relatively low FX fees depending on region and time of day (approximately 0.2% on weekdays in EEA/UK, approximately 0.7% on weekends, and up to 2%–2.5% in other regions). In Credit Mode, users pay interest on collateralized borrowings (starting from approximately 1.9%), while earning up to approximately 2% crypto cashback and continuing to generate interest on uncollateralized assets (up to approximately 13% annualized) — creating a “spend and earn simultaneously” model.

On cashback: Nexo Card offers up to 2% crypto cashback, payable in BTC (1%) or NEXO Token (2%). Cashback is credited instantly to the Nexo account and can be withdrawn or reinvested at any time. Cashback is tiered based on account level — the higher the level, the higher the rate — and monthly reward caps apply. Maintaining a sufficient asset balance (e.g., $5,000) is generally required to unlock full cashback benefits.

On security: Nexo Card integrates Mastercard’s security standards and provides real-time spending alerts and card freeze/unfreeze functionality through the Nexo App. The card can be fully managed in-app, including applying for a physical card, generating virtual cards, and viewing balance and cashback records.

Fiat24 Card

Fiat24 Card is a Mastercard virtual debit card issued by Swiss financial institution SR Saphirstein AG, operating on the Fiat24 dApp account system. Once users complete Fiat24 account verification, the card can be activated directly — no separate application process is required. The card is purely virtual (no physical card is offered) and has no PIN. It supports binding to Apple Pay, Google Pay, and Samsung Pay for both online and in-store payments.

In terms of fund management and usage mechanics, Fiat24 Card supports a multi-currency account model with balances in EUR, USD, CHF, and RMB. Users can enable the Direct Pay feature for individual currencies, ensuring that spending in a given currency deducts from the corresponding balance first, minimizing unnecessary FX conversion costs. When the balance is insufficient, the system automatically converts and pays using the default settlement currency.

On spending limits and tier structure: Fiat24 Card uses NFT-based tier levels (Standard, Premium, and Ultimate) to determine spending limits. For example, the Standard tier has a monthly limit of €20,000, while Premium and Ultimate tiers raise this to €200,000 and €1,000,000 respectively, catering to different scales of financial activity.

On risk controls and usage restrictions: Fiat24 Card restricts certain high-risk or compliance-sensitive transaction categories (such as gambling, financial services, and merchants in sanctioned regions). It supports 3D Secure (OTP email verification) to enhance online payment security. The card is fully controlled by the user’s on-chain account; if the private key or NFT is compromised, funds are at risk of misuse, and users are responsible for managing their own security.

Overall, Fiat24 Card represents a lightweight “on-chain fiat account + virtual card” payment solution. Its advantages include multi-currency direct payment, lower FX losses, and no need for a traditional bank account. However, the user experience and security are to some degree dependent on the user’s ability to independently manage on-chain assets and accounts.

PokePay Card

PokePay Card is a crypto payment card issued on the Visa network, available in both virtual and physical form. Users can top up with USDT, USDC, BTC, ETH, and other crypto assets, which are converted to USD or HKD within the platform for spending. The card covers a wide range of use cases: it can be linked to local apps such as Alipay, WeChat Pay, Meituan, and Taobao, as well as overseas subscription services like ChatGPT, and is compatible with Apple Pay, Google Pay, and PayPal — making it capable for both everyday domestic payments and cross-border spending.

KYC verification is required. Once funds enter the card system, they are held in custody by the platform, with 3DS and other security mechanisms in place to mitigate fraud risk. The fee structure is moderately detailed, including fixed fees for small transactions, approximately 1% in cross-border fees, and implicit exchange rate costs during crypto conversion. Overall, PokePay prioritizes accessibility, with strong performance in payment coverage and compliance — though it remains reliant on a centralized trust model, representing one of the most typical pathways in today’s mainstream crypto payment card market.

V-Card

V-Card is a crypto payment card launched by Bitcoin.com — essentially a prepaid debit card built on the Web3 wallet ecosystem, enabling spending and cash withdrawals worldwide through the Mastercard network. Users can top up with major crypto assets including BTC, ETH, USDT, and USDC, which are automatically converted to fiat at the time of payment, allowing them to spend at over 37 million merchants online and in-store, with global ATM withdrawal support. This design makes it a quintessential “bridge product” connecting crypto assets to the traditional payment network.

In terms of product structure, V-Card is deeply integrated with the wallet: users can hold assets in the Bitcoin.com Wallet prior to top-up, achieving a degree of self-custodial control. The card supports a multi-asset ecosystem including BTC, BCH, ETH, stablecoins, and the ecosystem token VERSE, with fee discounts and potential incentives for VERSE holders. However, once funds enter the card and payment is completed, settlement still relies on centralized custody and the fiat system.

BlockPurse

BlockPurse is a multi-currency virtual credit card (VCC) and global payment solution aimed at enterprise users, primarily serving cross-border e-commerce, digital advertising, and international business operations. The platform supports top-ups and settlements in multiple currencies including USD, HKD, and GBP, and provides multi-BIN virtual cards suitable for procurement on platforms such as Amazon, Alibaba, and AliExpress, as well as ad spend on Facebook and Google. It also covers logistics, SaaS subscriptions, PayPal binding, and other common enterprise payment scenarios.

On the product side, BlockPurse emphasizes enterprise-grade capabilities: rapid card issuance, multi-card management, and API integration. Users can issue cards in bulk, configure card parameters flexibly, and monitor cash flows and spending in real time through the platform. PCI DSS security standards and customizable risk control strategies are supported. On costs, the platform reduces FX losses through multi-currency cards and local currency settlement, combined with underlying liquidity optimization to minimize gas and settlement costs compared to traditional crypto payments.

Overall, BlockPurse is closer to an “enterprise-grade virtual card payment infrastructure” product, best suited for cross-border e-commerce sellers, advertising agencies, and globally operating teams managing multi-account, multi-scenario payment needs.

Note: As of the time of writing, the status of BlockPurse’s individual card application page cannot be confirmed through publicly available sources. Readers are advised to visit the official website directly to verify the latest availability before applying.

Wasabi Card

Wasabi Card is a crypto prepaid card product operating on major card networks (Mastercard and Visa), offering users worldwide the ability to convert digital assets into real-world spending power. Users top up their card account with USDT and convert it to a USD balance, enabling spending at any online or in-store merchant that accepts bank card payments. The card also supports binding to Apple Pay, Google Pay, and PayPal, as well as select local payment methods such as Alipay and WeChat Pay, covering use cases from e-commerce and ad spend to SaaS subscriptions and everyday purchases.

Rather than a single card product, Wasabi Card is segmented by use case into multiple types: the Promo (Media Buy) card for advertising spend and subscription payments, the SpendX card for personal spending and procurement, and the Physical card for in-store POS transactions and ATM withdrawals. A B2B card and API access for enterprise clients are also available, supporting bulk card issuance and payment management. This “multi-card type, scenario-driven” design positions Wasabi Card closer to payment infrastructure than a traditional consumer finance card. Different card types are issued on different networks (primarily Mastercard or Visa) to suit online versus offline payment needs.

On fees: there are no monthly or annual fees, but a one-time card issuance fee applies by type (approximately $10 for the Promo card, $39 for SpendX, and $299 for the physical card). Top-up fees exist and are subject to a minimum top-up amount, minimum balance, and card spending limit; non-USD transactions typically incur FX conversion fees. Withdrawals require a minimum amount and are subject to a time interval restriction (approximately 48 hours). Some card types require KYC verification. The overall model is centralized custody, with user funds managed within the platform account.

On risk controls: Wasabi Card’s provider centrally manages card limits, transaction caps, and eligible merchant categories, with the ability to restrict or decline transactions based on compliance and risk controls. Users can flexibly create or delete virtual cards to achieve fund isolation and risk management, with real-time balance viewing and spending management. The overall security framework is broadly comparable to traditional payment systems.

In summary, Wasabi Card is best characterized as a “centralized prepaid card plus scenario-driven payment tool,” emphasizing broad use-case coverage, flexible card usage, and global payment capability. It is well-suited for high-frequency online spending scenarios such as digital advertising, cross-border e-commerce, and digital service subscriptions. Users should nonetheless evaluate it against their own needs in terms of fund control, fee transparency, and platform dependency.

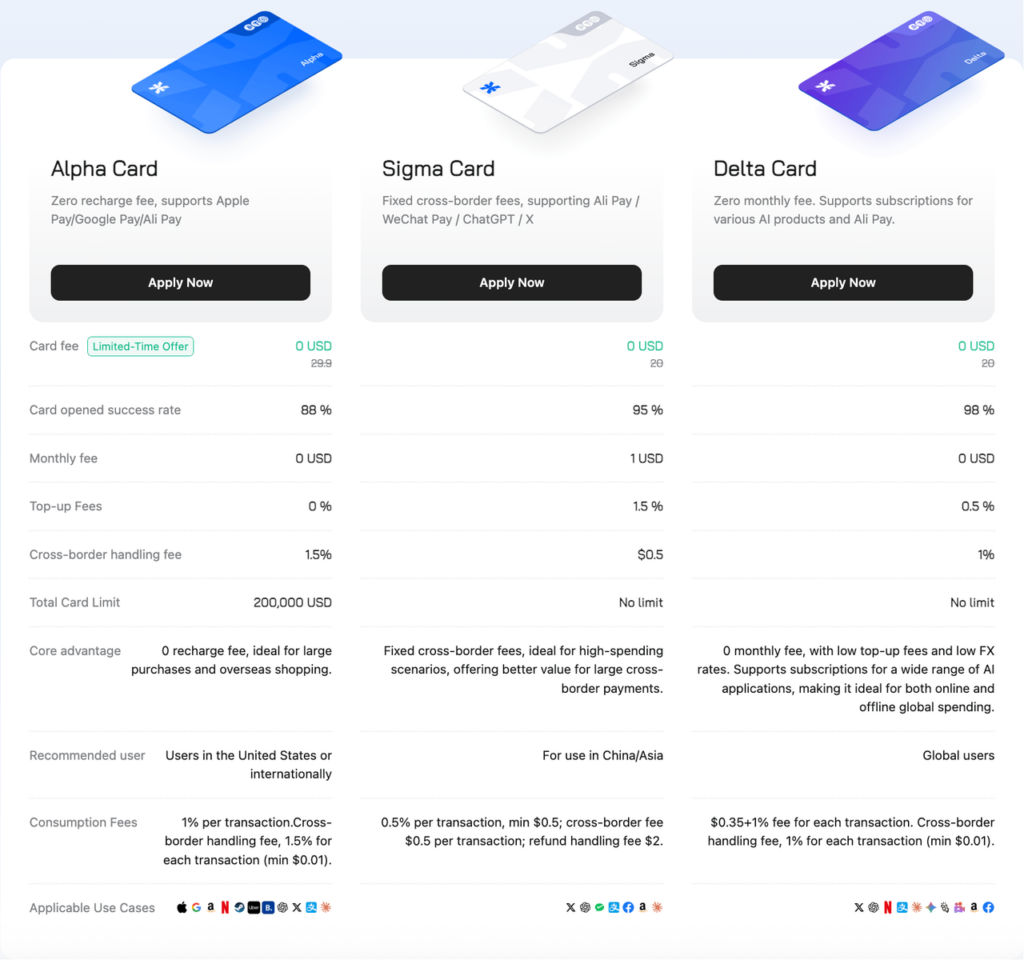

An Emerging Crypto Card Contender: BenPay Card

BenPay Card is a Web3 payment card built around an on-chain self-custodial architecture. Rather than offering a single card product, BenPay segments users by spending volume, frequency, and cross-border needs through three tiers — Alpha, Sigma, and Delta — enabling more precise matching to specific payment scenarios.

Across the key evaluation dimensions:

- Accessibility: No credit history, asset collateral, or geographic restrictions are required — users worldwide can apply with a passport or national ID. BenPay employs zkLogin technology, allowing users to securely log in to their on-chain wallet with a single tap via Google or Apple accounts, with no need to manage seed phrases. This significantly lowers the barrier to entry for everyday users entering Web3.

- Trust Model: Built on an on-chain self-custodial architecture, users retain full control over their assets at all times. Sensitive card information such as the card number and CVC can only be viewed through on-chain signature verification. A dynamic zero-knowledge proof (ZK) mechanism is incorporated to maximize user privacy while maintaining regulatory compliance. The technical foundation is built on the BenFen blockchain and has been audited by professional security firms including SlowMist.

- Cost Structure: The Alpha Card carries no top-up fees, monthly fees, or annual fees; the Delta Card likewise has no monthly fee. All transactions rely on BenFen’s extremely low gas fees (under $0.001) and a sponsored transaction mechanism, making the overall cost of use lower than most comparable products.

- Features:

- In addition to Apple Pay and Google Pay, BenPay supports local payment methods including Alipay and WeChat Pay, covering mainstream online and offline spending scenarios.

- The card can be used for AI subscriptions, streaming, cross-border e-commerce, and digital advertising across major platforms including Claude, ChatGPT, Netflix, Amazon, Uber, Booking, X, and Facebook.

- The Alpha Card has a maximum total spending limit of $200,000 per card with withdrawals available at any time, making it well-suited for ad spend and large procurement. The Sigma and Delta cards remove the total limit cap entirely, better serving high-frequency or high-value cross-border payment users.

- Beyond payment functionality, users can optionally enable on-chain yield generation, allowing idle card balances to earn returns continuously while unspent.

- User Experience: zkLogin delivers a login experience comparable to Web2 applications. Once the card is activated, it can be linked to mobile payment tools immediately — no complex on-chain operations required. At the community level, airdrop participation opportunities are available, which may appeal to early Web3 adopters.

Overall, BenPay Card represents a new category of crypto payment card built on a “self-custody + low cost + tiered use cases” model. Compared to the custodial model of CEX cards and the account-based systems of fintech cards, BenPay places greater emphasis on user asset control and capital efficiency. Compared to traditional DeFi cards, it more closely resembles a mature payment product in terms of user experience and payment scenario coverage. The product is still in an early stage, but demonstrates meaningful innovation in the direction of “direct payment from on-chain assets” with considerable room for growth.

Major Crypto Payment Cards Comparison Table

The table below summarizes key information for 16 crypto payment cards for easier side-by-side comparison. (Note: Some data may change over time and is provided for reference only.)

| Card Name | Approval Time | Spending Limits | Stability | Issuance Fee | Transaction Fees | Collateral | Use Cases | Notes |

| CoinJar Card | Instant | Daily max: $5,000; Max 25 transactions/day | Stable | $0 | 1% of transaction amount; 2.99% FX fee (at Mastercard rate) for non-AUD transactions; $27.50 per disputed transaction | None | Supports Apple Pay and Google Pay; spend crypto instantly and securely using your device | 1% transaction fee refunded as CoinJar Rewards points; physical card also $0 |

| Crypto.com Visa Card | A few hours to several business days | POS limit — Midnight: $10,000/day, $15,000/month; Ruby, Indigo/Jade, Icy/Rose, Obsidian: $25,000/day and month | Relatively stable | Midnight Blue: free, no subscription, no CRO staking required; all other tiers require CRO staking ($500–$500,000, typically 12-month lock) or paid subscription | 3% FX fee on all non-USD spending and ATM withdrawals (Midnight, Ruby, Jade/Indigo tiers) | CRO token staking | International use; Alipay/WeChat Pay not supported | Tiered benefits vary by level (including subscriptions and airport lounges); $4.95/month inactivity fee after 12 months with no cardholder-initiated financial activity |

| Nexo Card | Instant | Per transaction/per day: €10,000 / £9,000; Monthly: €60,000 / £54,000 | Stable | $0; virtual card requires min. $50 account balance to activate | FX conversion: 0.2% or 2% depending on local currency; additional 0.5% on weekend FX transactions | Yes — in Credit Mode, crypto holdings (BTC, ETH, NEXO, etc.) serve as collateral in Nexo account | Supports Apple Pay and Google Pay | Dual-mode card: switch seamlessly between Credit Mode (borrow against crypto) and Debit Mode (spend directly); cashback available when account holds $5,000+ in digital assets used in Credit Mode |

| Coinbase Card | Instant | Varies by customer tier | Relatively stable | $0 | No transaction fees; spread applies when buying, selling, or trading crypto | None | All Visa merchants globally; most international use cases | Coinbase One membership card offers 1%–4% crypto cashback |

| Fiat24 Card | Instant | Standard: €20,000/month, €10,000/day; Premium: €200,000/month, €100,000/day; Ultimate: €1,000,000/month, €500,000/day | Relatively stable | $0; requires a Fiat24 NFT (account NFT) | Top-up fee: Standard 1%, Premium 0.5%, Ultimate 0.25% | None | Supports Apple Pay, Google Pay, Samsung Pay | Minimizes conversion costs; designed for global travelers |

| BlockPurse | Instant | Due to API access and multi-currency settlement support, real-time limits vary — log in to the Blockpurse dashboard and check “Card Details” or “Limit Management” for your specific card | Uncertain | Typically $10 | Multi-BIN, multi-currency VCC; supports multiple currency top-ups; specific transaction fees require login to view | None | Cross-border e-commerce, advertising platforms, travel and logistics, software subscriptions, overseas study expenses | Crypto payment gateway |

| HyperCard | Virtual card applications suspended; physical card: notification within 1–2 weeks | Physical card: $1,000,000/month | Relatively stable | $269 | 3% top-up fee; 0.75% transaction fee; $70 annual fee | None | Visa / UnionPay / Mastercard global merchants; most online platforms domestic and international | Physical card requires passport; supports multiple crypto top-up options (BTC, ETH, USDT, etc.) |

| Bitget Card | A few minutes | Monthly limits by tier — Tier 1: $300,000; Tier 2: $500,000; Tier 3: $1,500,000; Tier 4: $3,000,000. Per-transaction limits — Tier 1: $10,000; Tier 2: $100,000; Tier 3: $500,000; Tier 4: unlimited | Relatively stable | $0 issuance fee; $0 annual fee | 0.9% per transaction | None | Google Pay and Apple Pay; international e-commerce and service platforms | $1/month inactivity fee if no transactions for 12 consecutive months (12-month period resets once activity resumes) |

| Bybit Card | Virtual card: instant; Physical card: 7–11 business days | Daily: $5,000; Monthly: $50,000; Annual: $250,000 | Relatively stable | Virtual card: $0; Physical card: $5 | FX fee: 1% (added on top of Mastercard rate); crypto conversion fee: 0.9% (added on top of spot trading fee) | None | Mastercard network globally | Funds are deducted from account balance at time of payment; remaining balance converted from crypto to fiat as needed |

| PokePay Card | Instant | Daily limit: HKD 100,000; Min. per transaction: HKD 0.1 | Relatively stable | Virtual: $5; Physical: $88 | 1% transaction fee; 1% currency conversion fee | None | ChatGPT Plus, Claude, Midjourney, OpenAI API, Netflix, YouTube Premium, Spotify, Disney+, Amazon, eBay, AliExpress, Shopee, Google Ads, Facebook Ads, PayPal, Google Pay, Stripe; Hong Kong Alipay binding for domestic online and offline QR payments | HKD Visa card only; no other card types offered |

| V-Card | Instant | €10,000/day; €100,000/month | Relatively stable | Standard: €75.00; Discounted: €49.99 (when paid with VERSE tokens) | Not explicitly disclosed | None | ChatGPT, OpenAI, Alipay, PayPal, Google Play, App Store, and other international platforms | Not available to US residents or citizens |

| Wasabi Card | Instant | Max top-up: $100,000 USD | Relatively stable | Promo: $10; SpendX: $39; Physical: $299; no monthly/annual fee | Top-up fees apply; specific rates undisclosed and vary by card type and scenario; no unified transaction fee publicly stated | None | Apple Pay; Mastercard-accepting global online platforms (e.g., Amazon, eBay) | Virtual and physical card options available |

| SafePal Card | 1–2 business days | Mastercard contactless: €1,600/day; other payment methods: €5,000/day; monthly limit equals daily limit | Relatively stable | $0 | $0 management/annual fee; top-up fee from 0.4%; withdrawal and deposit fee: 0.6%–1% | None | Global payment networks including PayPal, Apple Pay, Google Pay, and Samsung Pay | Earn points through top-ups, referrals, and SFP staking to unlock exclusive rewards |

| MetaMask Card | Instant | Virtual card: $10,000/transaction, $15,000/day; ATM: $1,000/transaction, $1,000/day. Metal card: $20,000/transaction, $30,000/day; ATM: $1,000/transaction, $5,000/day | Relatively stable | $0 | Virtual: $0 annual fee, 2% ATM withdrawal, 1% cross-border. Metal: $199 annual fee, first $1,200/month ATM free then 2%, zero cross-border fee | None | Pay via Apple Pay or Google Pay using mUSD, amUSD, wETH, EURe, GBPe, USDC, aUSDC, aBasUSDC, and USDT | 1 MetaMask Reward Point + crypto cashback per $1 spent; exclusive benefits from global partner network |

| RedotPay Card | Instant | Per transaction: $100,000; Daily: $1,000,000 | Relatively stable | Virtual: $10; Physical: $100 | Non-default currency: 1.2%; currency conversion fee: 1% | None | 130M+ merchants worldwide; enables stablecoin holders to spend globally via major card networks | ChatGPT4, Spotify, OpenAI, and Wise currently not supported |

| BenPay Card | Instant | Alpha: total limit $200,000 USD; Sigma and Delta: no total limit | Stable | $0 (limited-time) | Alpha: $0 monthly fee; $0 top-up fee; 1.5% cross-border fee; 1% per transaction; non-USD: 1.5% cross-border (min. $0.01). Sigma: $1/month; 1.5% top-up fee; $0.50 fixed cross-border fee; 0.5% per transaction (min. $0.50); non-USD: $0.50 fixed cross-border fee; $2 refund fee. Delta: $0 monthly fee; 0.5% top-up fee; 1% cross-border fee; $0.35 + 1% per transaction; non-USD: 1% cross-border (min. $0.01) | None | Alpha: Apple Pay, Google Pay, Amazon, Netflix, Steam, Uber, Booking, ChatGPT, Twitter/X, Alipay, Claude. Sigma: Twitter/X, ChatGPT, WeChat Pay, Alipay, Amazon, Claude. Delta: Twitter/X, ChatGPT, Netflix, Alipay, Claude, Gemini, Manus, PixVerse, Amazon, Facebook | Optional on-chain yield generation; idle balances can automatically earn returns |

Future Trends and Outlook

Taken together, existing crypto card products each have their strengths and serve different user segments. However, a fundamental tension runs through the entire space: products that prioritize convenience, low barriers, and rich features (such as high cashback and broad payment binding) tend to rely more heavily on centralized architectures, sacrificing transparency and user control; while products that more closely embody the Web3 ethos of decentralization tend to fall short in usability, cost efficiency, or feature breadth. Common shortcomings across the current crypto payment card landscape include:

- “Free” does not mean “zero cost”: Cards with no issuance fee or low upfront costs often carry costs at the top-up, conversion, or other stages. Users should pay close attention to the total cost of ownership (TCO).

- The trust model trade-off: The choice between the convenience of centralized custody and the peace of mind that comes from on-chain transparency and self-control is a fundamental decision for users. The latter remains a minority preference today, but it represents the directional value of Web3.

- KYC and geographic restrictions remain the primary barriers: Cards that genuinely offer global, low-barrier access without differentiation remain rare. Technologies such as zkLogin may change this.

- Cashback is not universal, and it comes at a price: High cashback rates typically come with specific holding requirements (as with exchange-affiliated cards) or carry underlying platform risk.

The end state of the crypto payment card space will not be defined by any single dimension. We believe the ideal future crypto payment card solution will require simultaneous improvement across multiple fronts:

- Trustworthy underlying architecture: Whether trust is established through technical means (such as on-chain transparency and zero-knowledge proofs) to enhance user control, or through rigorous compliance and auditing to build institutional-grade centralized trust, a solid security foundation is non-negotiable.

- Seamless user experience: The entire journey — from application and top-up to spending and account management — must be as smooth and intuitive as any Web2 application. Technologies like zkLogin will be important drivers of this.

- Competitive cost structure: This means not just low visible fees, but also minimizing hidden costs such as FX losses.

- Effective user incentives: Building on trust and experience, a well-designed cashback, points, or rewards system will be key to scaling the user base.

In summary, crypto payment cards are moving from early exploration toward mass adoption, with product forms continuously evolving — from custodial to non-custodial, from single-purpose spending tools to comprehensive financial services. Despite regulatory headwinds and market volatility, the vitality and pace of innovation in this space are remarkable. It is reasonable to expect that crypto payment cards will secure a meaningful place in the future financial landscape, serving as an important bridge between the traditional financial system and the crypto digital economy, and providing users around the world with richer and more convenient payment options.

Disclaimer

The product information, fee structures, and feature details referenced in this article are compiled from each project’s official website and publicly available materials as of Q1 2026, and are subject to change over time. For the most current fee rates, supported regions, and feature availability, please refer to the official disclosures of each respective card.

This article is intended solely for industry research and informational purposes, and does not constitute investment advice or a recommendation to use any specific product. Users should make independent judgments based on their own needs and risk tolerance before selecting any product.