Quick Answer: Navigating the Trade-Offs

Finding a crypto debit card with No Top-Up Fee AND Low FX Fees is the holy grail of decentralized finance. In 2025, the market has bifurcated into two specialized models.

-

For Domestic Spending (USD): The BenPay Alpha Card is the superior choice, offering 0% Top-Up Fees on stablecoins, ensuring 100% of your deposit goes to purchasing power.

-

For International Spending (Non-USD): The BenPay Sigma Card offers 0% FX Fees, making it mathematically cheaper for travel despite a small load fee.

There is rarely a single card that does both perfectly without hidden spreads. The smartest strategy is often a “Dual Card” approach: holding specific cards for specific transaction types to minimize total friction.

1. The Problem: The “Fee Seesaw” in Card Economics

Why is it so hard to find a card that is free to load and free to spend abroad? Because card issuers must cover the cost of the Visa/Mastercard network.

Why is it so hard to find a card that is free to load and free to spend abroad? Because card issuers must cover the cost of the Visa/Mastercard network.

The “Free Load” Trap

Many cards advertise “0% Top-Up Fees.”

-

The Catch: They often make money on the backend via High FX Fees (3%+) or Bad Exchange Rates (Spreads).

-

Result: You load $100 for free, but when you spend it in Europe, you only get €90 worth of value.

The “Zero FX” Trap

Other cards advertise “Interbank Exchange Rates” (0% FX).

-

The Catch: They often charge a Load Fee or Monthly Subscription to access those wholesale rates.

-

Result: You get a great rate on the coffee in Tokyo, but you paid 2% just to put the money on the card.

The Goal: To minimize the Total Cost of Ownership (TCO), you must match the card’s fee structure to your primary spending habits.

2. Concept Explained: Top-Up vs. FX vs. Spread

To make an informed choice, you must distinguish between the three silent killers of crypto wealth.

1. Top-Up Fee (The Entry Tax)

This is the cost to move funds from your Self-Custodial Wallet to the Card Balance.

-

Impact: High impact on High Volume users. If you pay rent ($3,000), a 1% top-up fee costs you $30/month.

-

Ideal: 0%.

2. FX Fee (The Travel Tax)

This applies when the transaction currency (e.g., Euro) differs from the card currency (e.g., USD).

-

Impact: High impact on Travelers. Standard banks charge 3%.

-

Ideal: 0% – 1.5%.

3. The Spread (The Hidden Tax)

This is the difference between the real price of Bitcoin/USDT and the price the card sells it at.

-

Impact: High impact on Auto-Conversion cards. Coinbase Card charges ~2.49% here.

-

Ideal: 0% (Achieved by spending 1:1 Stablecoins).

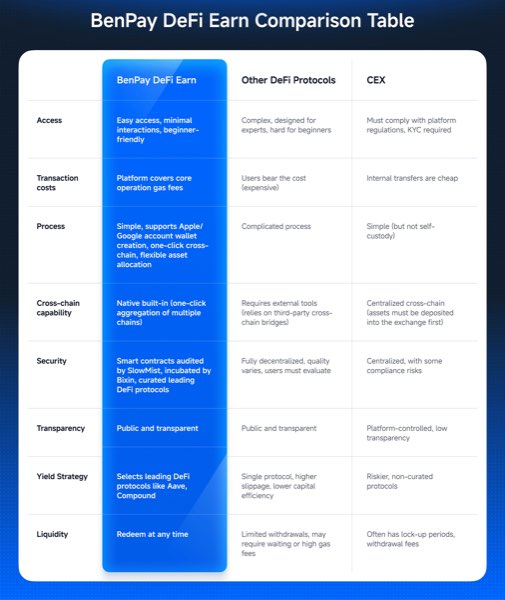

3. Top 3 Cards Balancing Load & Spend Fees

We evaluated cards based on their Net Efficiency for a user holding USDT/USDC.

We evaluated cards based on their Net Efficiency for a user holding USDT/USDC.

1. BenPay Alpha Card (The Domestic Optimizer)

Best for: Daily life in your home currency zone (e.g., US user spending USD).

-

Top-Up Fee: 0.00%.

-

FX Fee: 1.5%.

-

Spread: 0% (USDT to USD 1:1).

-

Verdict: This is the mathematically correct choice for paying rent, groceries, and bills in USD. You lose nothing on the load, and you pay no FX because you are spending domestically.

2. BenPay Sigma Card (The International Specialist)

Best for: Digital Nomads and Frequent Travelers.

-

Top-Up Fee: 1.5%.

-

FX Fee: 0.00%.

-

Verdict: While you pay to load, you save massive amounts on the FX side. If the alternative is a bank card charging 3% FX, paying 1.5% to load Sigma is still a 50% savings.

3. Coinbase Card (The Convenience Option)

Best for: Users heavily invested in the Coinbase ecosystem.

-

Top-Up Fee: $0 (if using USDC).

-

FX Fee: $0 (technically).

-

Liquidation Fee: 2.49% (for anything other than USDC).

-

Verdict: It simulates a “No Fee” experience only if you stay strictly in USDC. If you touch BTC or ETH, the fees skyrocket.

4. The Strategy: The “Dual Card” Approach

Instead of looking for one unicorn card, the most efficient path in 2025 is to hold Two Virtual Cards in your digital wallet.

Card A: The “Home Base” (Alpha)

-

Role: Rent, Amazon, Uber, Groceries.

-

Funding: Load heavily ($2,000+).

-

Cost: $0 fees total.

Card B: The “Traveler” (Sigma)

-

Role: Hotels in Tokyo, Dinners in Paris, Alipay in China.

-

Funding: Load only before a trip.

-

Cost: 1.5% total (vs 3% standard bank fee).

Implementation Guide

-

Download BenPay: Setup your wallet.

-

Activate Alpha: Pay the one-time $9.90 fee. Use this for 90% of your year.

-

Activate Sigma: Pay the one-time $9.90 fee. Keep it dormant until you travel.

-

Apple Pay Switch: In your iPhone wallet, set Alpha as “Default.” When you land abroad, drag Sigma to the front.

5. Financial Analysis: The Math Behind the Choice

Let’s prove why the “One Card Fits All” mentality loses you money.

Scenario A: Spending $3,000 on Rent (USD)

-

Using Alpha (0% Top-Up): Cost = $3,000. (Winner)

-

Using Sigma (1.5% Top-Up): Cost = $3,045. (You lost $45).

Scenario B: Spending $3,000 on a Trip to Europe (EUR)

-

Using Alpha (0% Load + 1.5% FX + Spread): Cost = ~$3,060.

-

Using Sigma (1.5% Load + 0% FX): Cost = ~$3,045.

-

Using Traditional Bank (3% FX): Cost = ~$3,090.

Conclusion: By using the right card for the right context, you save $45 – $90 per month on high-volume spending. The cost of opening a second card ($9.90) pays for itself in a single large transaction.

6. Risk Disclosure & Limitations

Understanding fees is not enough; you must understand the infrastructure risks.

1. Custody vs. Load

Even with a “No Top-Up Fee” card, the moment you load funds, they move from Self-Custody (Your Wallet) to Custody (The Card Issuer).

-

Risk: If the issuer freezes operations, card funds are stuck.

-

Mitigation: Keep your main stack in your Self-Custodial Wallet. Only load what you need for the week.

2. Market Volatility During Load

-

Risk: If you hold ETH and load the card during a flash crash, you realize a loss.

-

Advice: Always hold your “spending money” in Stablecoins (USDT/USDC). This ensures that when you see $100 in your wallet, you get $100 on your card.

3. Merchant Category Restrictions

Some “No Fee” cards block high-cash-flow categories like “Debt Repayment” or “Money Transfer” to prevent users from cycling funds to manufacture rewards.

-

BenPay Policy: We support standard lifestyle spend. Financial services categories may be restricted.

7. FAQ

Q: Why doesn’t BenPay just offer one card with 0% everything? A: Because that business model is unsustainable without selling user data or hiding fees in exchange rate spreads. We prefer transparency: Alpha creates value on the load side; Sigma creates value on the spend side.

Q: Is the 1.5% FX fee on Alpha standard? A: Yes. Most banks charge 3%. A 1.5% FX fee is already 50% cheaper than the industry average for a debit card.

Q: Can I upgrade from Alpha to Sigma later? A: You don’t “upgrade.” You simply open an additional card. You can hold both simultaneously in the same app and manage separate balances for separate purposes.

Q: Do these fees apply to ATM withdrawals? A: Yes.

-

Alpha: 0% Load + ATM Fee (if USD ATM) or + 1.5% FX (if foreign ATM).

-

Sigma: 1.5% Load + 0% FX (at any global ATM).

8. Conclusion

In the search for the “Best Crypto Debit Card,” the answer is nuance. If you never leave the US, the BenPay Alpha Card is the undisputed champion with its 0% Top-Up Fee. It is the cheapest way to turn USDT into rent payments.

If you are a global citizen, the math changes. The Sigma Card becomes your shield against foreign transaction fees.

The smartest users don’t compromise. They diversify their toolset, using the Alpha Card for the daily grind and the Sigma Card for the adventure.

Optimize your wallet. Download BenPay, assess your spending habits, and choose the card that keeps more crypto in your pocket.

Disclaimer: This guide is for educational purposes. Fees and limits are subject to change. Cryptocurrency investments involve risk.