According to industry research, nearly 93% of freelancers hope to receive at least part of their income in cryptocurrencies or stablecoins (such as USDT/USDC), and blockchain industry salary data show that the adoption of stablecoin salaries accelerated in 2025. Meanwhile, the use of stablecoins such as USDC for on-chain payments has increased by more than 300% year-on-year, indicating a rapid expansion of their real-world adoption.

However, a core issue remains unresolved: How can USDT/USDC income be used directly for daily consumption?

A crypto debit card for freelancers bridges that gap — turning stablecoin income into everyday spending power, just like cash.

This guide explains how it works, why a stablecoin debit card is becoming essential for freelancers/remote workers, and how options like the BenPay Card are designed specifically for this use case.

Why Freelancers Are Switching to USDT & USDC

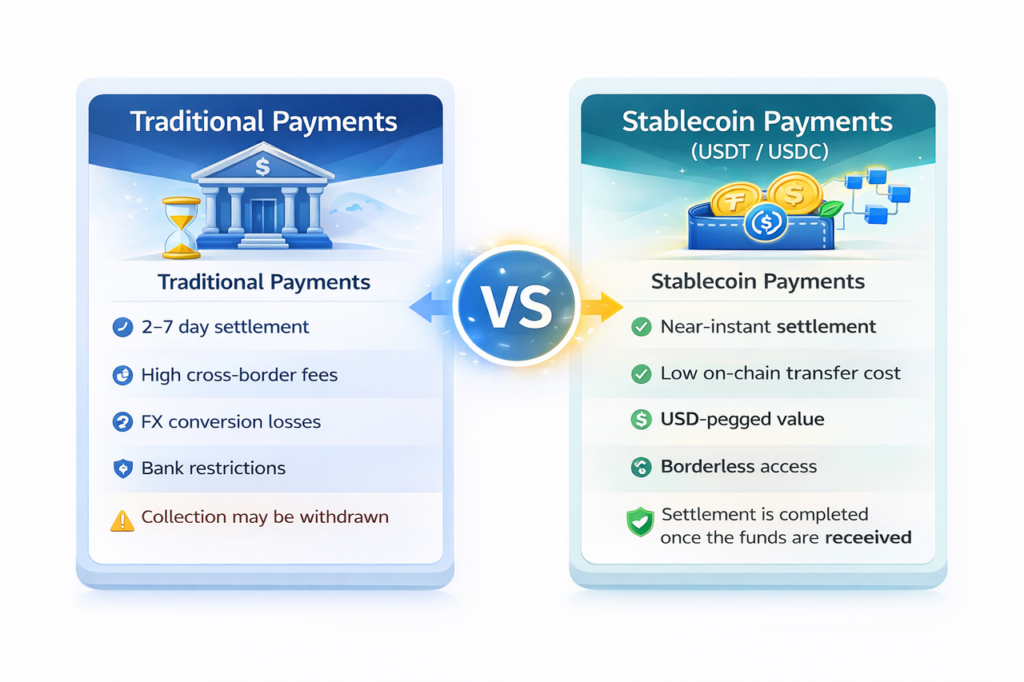

Freelancers increasingly prefer stablecoin payments over bank transfers because:

| Traditional Payments | Stablecoin Payments (USDT/USDC) |

| 2–7 day settlement | Near-instant settlement |

| High cross-border fees | Low on-chain transfer cost |

| FX conversion losses | USD-pegged value |

| Bank restrictions | Borderless access |

| Collection may be withdrawn | Settlement is completed once the funds are received |

For developers, designers, marketers, Web3 contributors, and remote contractors, USDT and USDC function as global digital dollars. But earning in stablecoins is only half the equation. Spending is the other.

What Is the Best Crypto Debit Card for Freelancers?

A crypto debit card lets freelancers:

- Receive client payments in USDT/USDC

- Store funds in a self-custody or on-chain wallet

- Convert crypto to fiat at the moment of spending

- Pay anywhere normal debit cards are accepted

So your workflow becomes:

Client → USDT/USDC → On-chain wallet → Card → Shop, rent, SaaS tools, flights or others

It’s the missing link between Web3 income and real-world expenses.

Key Features Freelancers Should Look For

Not all crypto cards are built for freelance income. Here’s what actually matters:

1. Stablecoin Support (USDT / USDC): Your card should natively support stablecoins — not force constant token swaps.

2. Low Top-Up Fees: Freelancers often move money frequently. High deposit fees destroy margins.

3. Cross-Border Friendly: You may live in one country, work in another, and travel between both.

4. Digital Wallet Compatibility: Apple Pay, Google Pay, Alipay, and WeChat Pay, these make your crypto circulate like cash.

5. No Heavy Monthly Costs: Freelance income fluctuates. Fixed card fees can become a burden.

Why This Matters for Freelancers

Pay for Work Tools, Use USDC/USDT earnings to pay:

- Adobe, Figma, Notion

- Cloud hosting

- AI tools

- Marketing platforms

Travel-Friendly Income: Freelancers working remotely can:

- Book flights

- Pay hotels

- Spend overseas

Without moving money through banks first.

Keep More of Your Income: Lower fees compared to:

- Wire transfers

- PayPal currency spreads

- International card FX markups

Means higher net earnings.

BenPay Card: Crypto Payment Card Built for Freelancers

For freelancers, the value of BenPay Card lies not only in “being able to spend stablecoins”, but also in its adaptation to the financial structure and working style of freelancers.

The transactions of freelancers often have these characteristics:

- Clients are scattered, and many of them are one-time collaborations

- Frequent temporary receipts are required

- There are diverse cooperation platforms (remote platforms, Web3 projects, overseas clients)

- They do not want to frequently provide bank account information

The traditional bank transfer process requires information such as account name, address, and SWIFT code, which is complex and slow for cross-border transactions. BenPay Card uses on-chain addresses for receiving payments. The recipient only needs to transfer USDT/USDC to complete the payment. It is particularly suitable for scenarios such as one-time project settlement, short-term outsourcing, and cross-platform order taking.

BenPay Multi-Card Comparison

The BenPay Card ecosystem offers a variety of card designs, allowing you to choose one based on your location and spending habits. This comparison table shows how different BenPay Cards fit different freelance use cases globally.

| Feature | Alpha Card | Sigma Card | Delta Card |

| Card Opening Fee | 9.9 BUSD | 9.9 BUSD | 9.9 BUSD |

| Monthly Fee | $0 | $1 | $0 |

| Top-Up Fee | 0% | 1.50% | 0.50% |

| Cross-Border Fee | 1.50% | $0.5 per transaction (Mainland China rule) | 1% |

| Total Card Limit | $200,000 | Unlimited | Unlimited |

| Payment Support | Apple Pay / Google Pay / AliPay / WeChat Pay | AliPay / WeChat Pay / ChatGPT / X | Apple Pay / Google Pay / AliPay |

| Core Advantage | Zero top-up fee, ideal for large purchases | Fixed cross-border cost for high spenders | Zero monthly fee + low FX & top-up costs |

| Recommended Users | US-based & global freelancers | Asia-focused freelancers | Digital nomads & global freelancers |

On-Chain Yield: Hidden Advantage of Freelancers

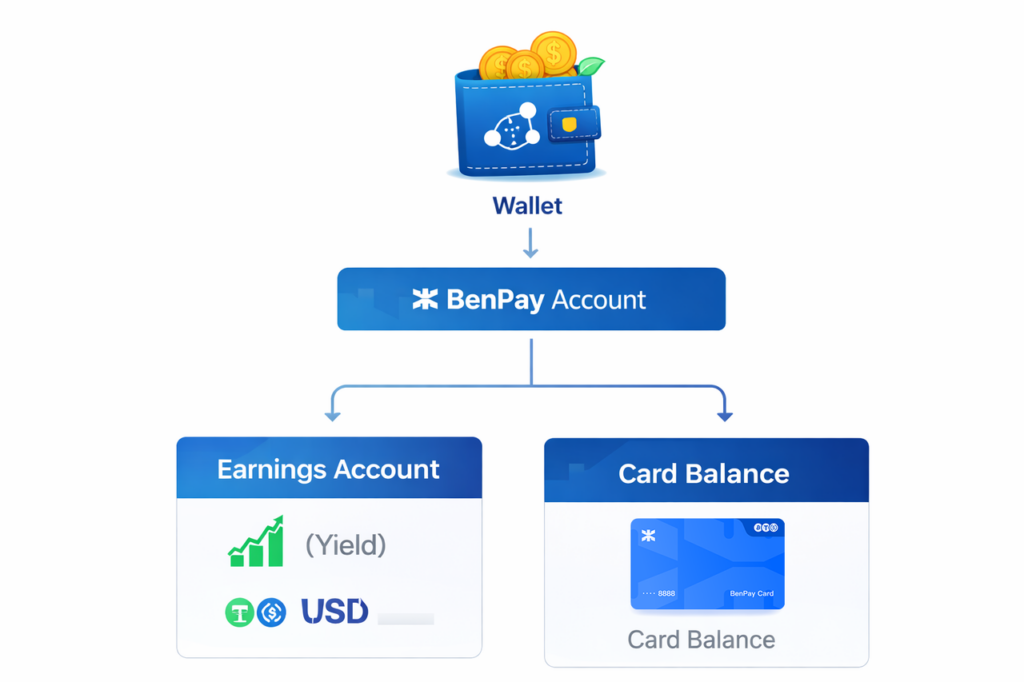

Freelancers’ income is irregular, often following a pattern of “concentrated funds arriving and dispersed expenditures“, and some of their funds are often in a short-term idle state. The on-chain interest-generation function of the BenPay Card enables these funds to participate in DeFi yield strategies, improving utilization efficiency without affecting the ability to withdraw funds.

Users can deposit USDT/USDC in the balance of their BenPay Card account (earnings account) to earn on-chain earnings. When there is a need for consumption, it will be transferred to the balance of the card (payment account) for daily expenses. This forms a two-tier capital model:

- Idle funds are used for on-chain earnings

- Daily consumption funds maintain payment liquidity

This structure makes the encrypted debit card no longer merely a payment tool, but a tool that combines liquidity management and yield management.

A small tip: Keeping the portion of funds that have not been used for a long time in the card account balance to generate interest while maintaining the balance of the card to cover daily expenses is a more efficient way to allocate funds.

Privacy Layer: Encrypted payment privacy design for freelancers

For freelancers who receive payments in stablecoins, the issue is not only how to earn and spend money, but also how to manage the visibility of funds.

In the traditional banking system, transaction records are held by multiple intermediary institutions. However, ordinary on-chain transfers may be publicly displayed on block browsers for a long time. As income, savings, and daily expenses all move on-chain, transaction visibility itself becomes a resource that needs to be managed.

BenPay’s privacy payment system incorporates native privacy capabilities at the payment layer, helping freelancers better manage their financial information within a compliance framework:

- Native privacy at the chain layer: Privacy functions are directly built at the bottom layer of the blockchain, rather than simply mixing coins or taking detours for processing

- Amount Hidden On-Chain: Transactions occur, but the amount of information is not disclosed, protecting the scale of income from external speculation

- Compliance-friendly: While protecting personal financial visibility, it supports legal payments and business compliance

This is not for “hiding transactions” but for building professional financial boundary management capabilities. When income, savings, and daily expenses are all conducted on-chain, controlling the visibility of information becomes an important part of modern on-chain financial management.

How BenPay Card Works in Practice

Step 1: Client pays you in USDT or USDC, and the payment is sent to your BenPay self-custodial wallet address. Step 2: Funds arrive in your on-chain wallet, and you can check the balance. This stablecoin income will not be held by banks or exchanges and is always under your control. Step 3: Transfer wallet funds to the balance of the card account → Choose independently whether to start participating in on-chain income.

Step 4. When you need to make a purchase → Transfer to the card balance (select the corresponding card within the BenPay app, such as Alpha/Sigma/Delta).

Step 5. When you make a payment with a BenPay card, either offline or online, the system will convert the stablecoin into the corresponding fiat currency at the moment of consumption to complete the transaction. You don’t need to manually exchange it or go to an exchange to operate.

To the merchant, it looks like a regular card transaction. To you, it’s on-chain freelance income becoming real-world spending and earning power.

Final Thoughts

If you’re a freelancer earning money in USDT or USDC, a crypto debit card is no longer optional — it’s operational infrastructure.

Solutions like BenPay Card let you:

- Receive stablecoin income seamlessly

- Avoid banking friction

- Spend globally without delays

- Manage costs effectively

- Earn on-chain yield while keeping funds spend-ready

Start by setting up a BenPay self-custodial wallet, receiving a small test payment in USDT/USDC, and try topping up your card to experience the complete workflow of on-chain income → on-chain interest generation → actual expenditure.